Croatia is joining the global shift toward Continuous Transaction Controls (CTC).

If you do business in Europe, you’ve seen this movie before. Governments want real-time visibility into transactions to close the VAT gap. Italy did it. Now Poland, Belgium, and Croatia are rolling out similar reforms and the pattern is spreading globally.

In Croatia, that next chapter is Fiscalization 2.0: a new B2B e-invoicing mandate, paired with expanded reporting requirements that bring B2B invoices, transaction and payment data into the tax authority’s line of sight.

The system has roots in Croatia’s “Fiscalization 1.0,” which required real-time reporting of B2C cash and card receipts. But Fiscalization 2.0 is different: it takes fiscalization beyond point-of-sale receipts and into B2B e-invoicing.

Here is what is changing and why you need to pay attention.

Key Milestones

The rollout is aggressive with milestones defined in Croatia’s Law on Fiscalization:

September 1, 2025: Pre-implementation begins

- The law enters into force.

- The Tax Administration opens a test environment for access points, information brokers, and taxpayers.

January 1, 2026: Mandate goes live

- B2B e-invoicing becomes mandatory for all VAT-registered taxpayers for domestic transactions.

- Fiscalization expands to B2C invoices paid via transaction accounts, including bank transfer and similar methods.

January 1, 2027: Country wide coverage

- Non-VAT taxpayers (e.g., small businesses and flat-rate craftsmen) must begin issuing e-invoices.

The Key Requirements

Scope of Application

The Act applies broadly to all taxable persons established in Croatia. This includes any legal or natural person registered for VAT, as well as smaller entities liable for income or profit tax, and public bodies. However, there is a critical distinction for international business: Non-resident entities are generally out of scope. If you are a foreign company registered for VAT in Croatia but you do not maintain a Permanent Establishment in the country, you are not mandated to issue compliant e-invoices under this specific law.

Transactional Scope

The mandate distinguishes transactions based on the status of the buyer and the nature of the supply.

- In Scope:

- Domestic B2B: Supply of goods/services between two Croatian established taxpayers.

- Domestic B2G: Supply to public bodies.

- Out of Scope:

- Cross-Border: Intra-community supplies and exports to third countries are currently exempt from the e-invoicing mandate.

- Certain activities defined in Law, such as the sale of tickets in passenger transport, lottery services, and banking/insurance services, are exempt from the fiscalization obligation

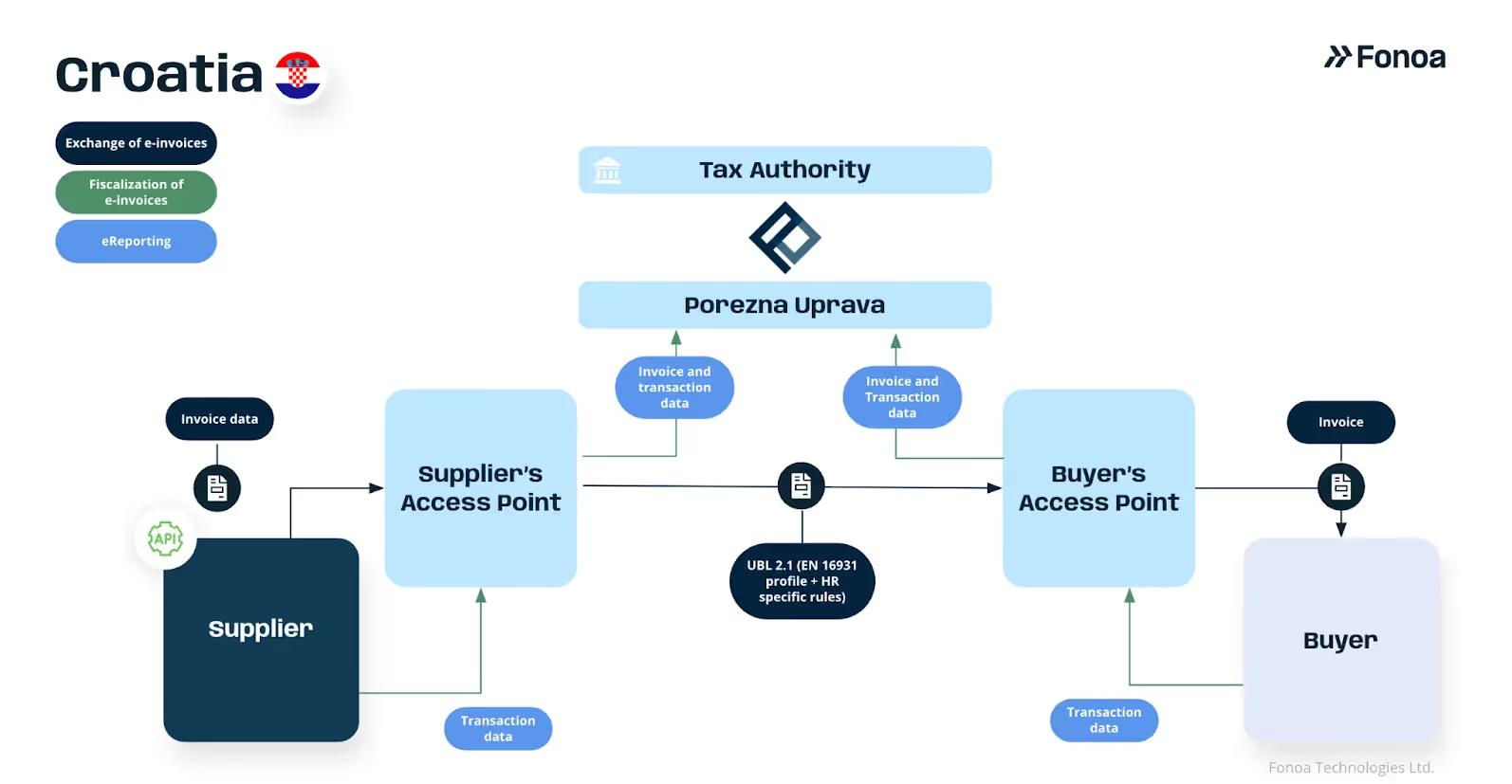

The B2B E-Invoicing Model: Decentralized Exchange with Centralized Reporting

Croatia has chosen a decentralized CTC model, often referred to as the “5-corner model.” Unlike centralized clearance systems such as Italy’s SDI or Poland’s KSeF, where the tax authority sits in the middle of invoice delivery, Croatia takes a different approach: the market handles the exchange, while the tax authority receives the relevant data for monitoring and reporting.

This structure is illustrated in the workflow below: invoices flow between trading partners through their service providers (Access Points), while invoice and transaction data is reported to the Tax Administration (Porezna uprava) in parallel.

The Exchange Workflow (E-Invoice Delivery)

The actual delivery of the e-invoice happens directly between service providers, keeping the market open and competitive.

The supplier generates an invoice in their ERP or billing system. To send it, they must know where to deliver the e-invoice. This is handled through the Address Management System (AMS).

- The Supplier’s Access Point (AP) queries the AMS using the Buyer’s OIB (Tax ID).

- The AMS returns the URL of the Buyer’s Metadata Service (MPS).

- The Supplier’s AP queries the MPS to retrieve the Buyer AP’s technical endpoint and public key.

This dynamic discovery mechanism removes the need for static bilateral connections between every provider, creating an interoperable network similar to Peppol, but managed locally.

Once the endpoint is discovered, the full e-invoice (UBL 2.1 XML) is wrapped in an AS4 envelope and transmitted directly from the Supplier’s AP to the Buyer’s AP. This protocol ensures message security and non-repudiation.

The Fiscalization Workflow

In parallel to the exchange, both parties must report data to the Tax Administration. This “dual reporting” creates a closed audit loop (as shown in the workflow above).

1) Issuer fiscalization (accounts receivable)

At the time of issuance, the Supplier’s service provider extracts a defined subset of invoice and transaction data and sends it to the Tax Administration’s fiscalization system.

- Validation: The Tax Administration validates the digital signature, certificate validity (including the OIB), and schema/business rules.

- Response: If valid, the Tax Administration returns a success message.

Unlike B2C fiscalization, there is no JIR printed on the B2B invoice, and the invoice is not invalid if such an identifier is missing. This step is a reporting obligation that must be fulfilled at the time of issuance.

2) Recipient Fiscalization (accounts payable)

Upon receiving the e-invoice, the Buyer's AP extracts the relevant data and sends a fiscalization message to the Tax Administration.

- Purpose: This confirms to the tax authority that the invoice was successfully delivered and received. It closes the audit loop, matching the invoice data reported on the AR and AP flows.

- Timing: The recipient has a 5 working day window to perform this fiscalization step.

E-Reporting Scenarios (Exceptions & Lifecycle)

Not every commercial event fits neatly into the “issue → send → fiscalize” workflow. The e-reporting layer captures exceptions and lifecycle events so the Tax Administration has a complete view of transaction status and VAT liability.

- Invoice rejection: If a buyer refuses an e-invoice (e.g., due to incorrect price or quantity), they must report the status change to the Tax Administration. This helps prevent discrepancies where the issuer declares output VAT but the buyer rejects the liability.

- Payment status: Issuers must report when an e-invoice is paid, supporting visibility into settlement and cash flow.

- No AMS match (fallback flow): If a buyer cannot be found in the AMS, the supplier may issue a paper invoice but must still report the transaction data to the Tax Administration.

Challenges

Below are some of the key challenges businesses face when implementing Fiscalization 2.0:

- Different rules for B2C: B2C requirements remain distinct from B2B. For consumer transactions, fiscalization must happen in real time, and you need the clearance from TA to have a valid fiscal receipt. The key here is scoping: make sure you understand which flows you need to support (B2B, B2C, or both), and choose a service provider that can cover the full scope.

- Fiscalization on both AR and AP: Unlike most countries where only the seller reports, Croatia requires both the issuer (AR) and the recipient (AP) to fiscalize the invoice. Operationally, this means there is an additional reporting layer in the Access Point flow on both sides, not just for invoice issuance, but also for reporting lifecycle events such as rejections to the TA.

- Croatian CIUS (EN 16931 with local “flavours”): Croatia builds on EN 16931 as the baseline, but adds local requirements through the Croatian CIUS. Examples of Croatia-specific requirements include fields such as the operator OIB, invoice time, and Croatia-specific exemption codes for VAT-exempt and out-of-scope invoices.

- Line-level product classification: For B2B e-invoices, every invoice line must include a 6-digit KPD 2025 classification code (with the exception of advance invoices). Without this data point, invoices cannot be exchanged and fiscalized successfully, so product classification becomes a hard dependency for go-live readiness.

- Single receiving Access Point: While you can use multiple providers to send invoices, the system requires you to register one receiving Access Point per identifier in the Address Management System (AMS). For example, an OIB can be mapped to a single receiving AP. If you use additional identifiers (such as GLN), those identifiers can be registered with a different receiving AP, so it’s important to understand how your business identifies entities and routes inbound invoices.

How Fonoa helps with Fiscalization 2.0

Fiscalization 2.0 is complex because it combines a new B2B e-invoicing mandate with an expanded B2C fiscalization regime. Many providers cover only one side of the equation but Fonoa supports both through a single solution.

We’re officially accredited as an Information Intermediary by the Croatian Tax Administration, meaning we’ve passed the required technical and security assessments and appear on the official list of certified brokers. And we’re not new to Croatia: we’ve supported high-volume, real-time B2C fiscalization for years and are now bringing the same expertise to B2B, including AS4-based e-invoice exchange.

Instead of building a Croatia-specific integration, you can connect once to Fonoa’s global API while we handle the local requirements so your team can stay focused on your core product.