Nexus refers to the connection or presence that a business has in a particular state that gives that state the authority to require the business to collect and remit sales tax on its taxable sales in that state. In the context of U.S. sales tax, nexus is established when a business has a physical presence in a state (physical nexus), such as a store, warehouse, or employees, or when it engages in certain types of economic activity in that state (economic nexus).

If a business has no nexus in a particular state, then that state cannot require the business to charge sales tax.

Economic nexus typically arises when a business exceeds certain thresholds of sales, transactions, or other economic activity within a state, even if the business does not have a physical presence in that state. The concept of economic nexus has become increasingly important with the rise of e-commerce and online sales, as it allows states to impose sales tax obligations on out-of-state businesses that may not have a physical presence in the state.

Each U.S. state has its own rules on what constitutes economic nexus, which can vary considerably. We have detailed the most important information needed to complete this calculation:

- Sales threshold: Economic nexus can be triggered by making a certain value of sales in a state during a given time period. Some states also have a trigger based on the number of transactions (generally 200). A few states require that both triggers are met before the nexus is created.

- Reference period: Most states look at the calendar year when determining whether the economic nexus threshold has been reached (e.g. January 1, 2022 to December 31, 2022). However, some states have different reference periods.

- Transactions made through a registered marketplace facilitator excluded: To calculate nexus, some states allow sellers to exclude any sales made through a registered marketplace facilitator (e.g. a marketplace facilitator registered for sales tax who calculates, collects, and remits sales tax on the seller’s behalf). Most states however require that sellers include both sales made directly to customers and sales made to customers through a marketplace facilitator when performing a nexus calculation.

- Transactions made to a reseller excluded: Some states allow sellers to exclude sales made to resellers when performing a nexus calculation. As a general rule, sales made to resellers holding a valid exemption certificate are not subject to sales tax.

- Limited to certain transaction types: Some states allow sellers to exclude certain types of sales when performing a nexus calculation, for example, non-taxable sales or sales of anything other than tangible personal property (TPP).

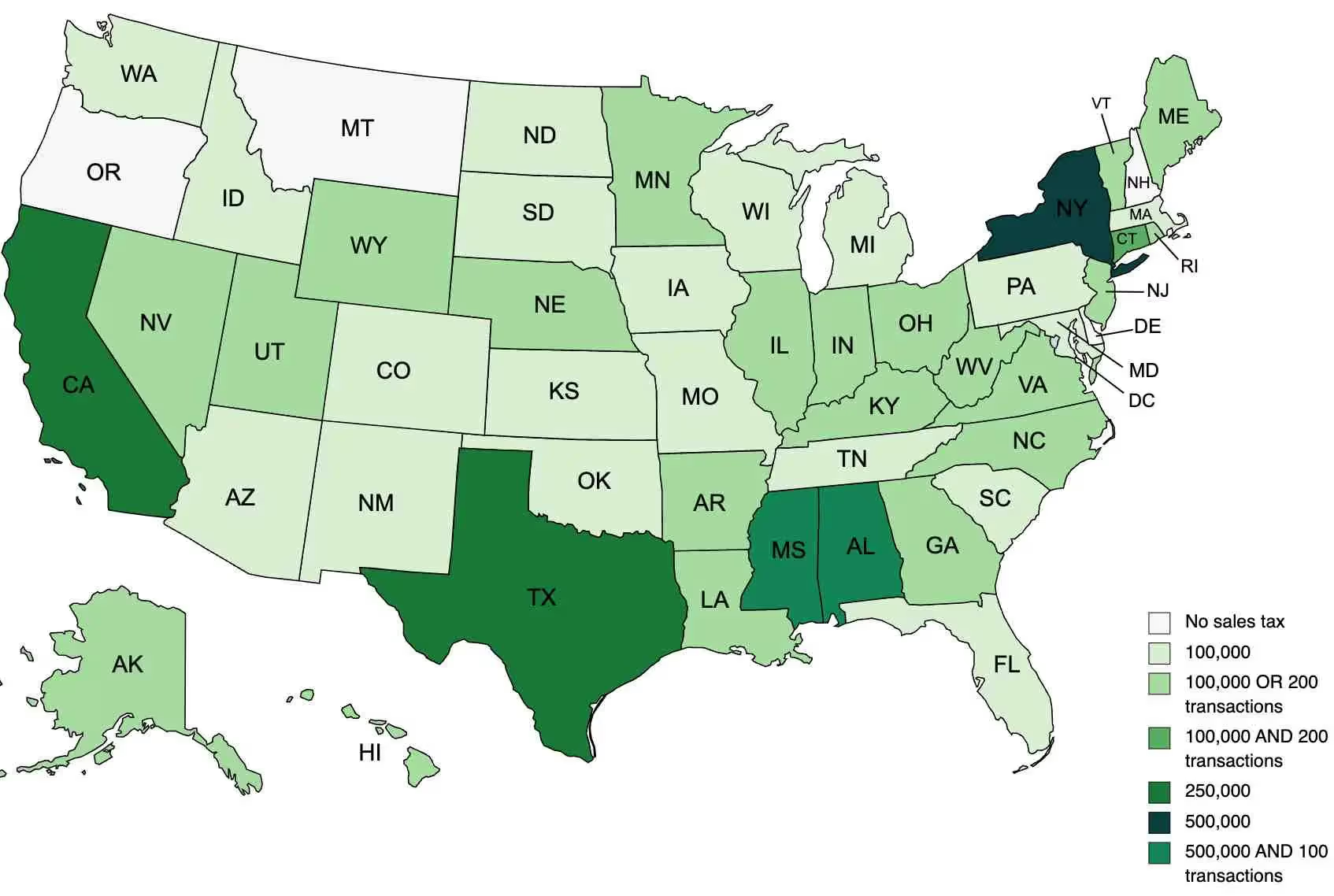

Alabama

- $250,000 in sales during the prior calendar year

- Transactions made through a registered marketplace facilitator excluded: Yes

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: TPP only

- Source

Alaska

- Before January 1, 2025: Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- As of January 1, 2025: Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Arkansas

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: Yes

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: Taxable transactions only

- Source

Arizona

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: Yes

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

California

- Over $500,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: TPP only

- Source

Colorado

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: TPP only

- Source 1, Source 2

Connecticut

- Over $100,000 in sales AND 200 transactions during the 12 month period ending 30 September (e.g. October 1 2021 to September 30 2022)

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: No

- Source

DC

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: Yes

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Delaware

No sales tax

Florida

- Over $100,000 in sales during the prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: Taxable TPP only

- Source

Georgia

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: TPP only

Hawaii

- $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Idaho

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Illinois

- $100,000 in sales OR 200 transactions during a 12 month period ending any quarter (e.g. July 1, 2021 to June 30, 2022 or April 1, 2022 to March 31, 2023)

- Transactions made through a registered marketplace facilitator excluded: Yes

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: TPP only

- Source 1, Source 2

Indiana

- Over $100,000 in sales transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Iowa

- $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Kansas

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Kentucky

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: TPP and digital property only

- Source

Louisiana

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Maine

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: TPP, taxable services, and products transferred electronically only

- Source

Maryland

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: TPP + taxable services only

- Source

Massachusetts

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Michigan

- Over $100,000 in sales during the prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Minnesota

- Over $100,000 in sales OR 200 transactions during any 12 calendar month period

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: No

- Source 1, Source 2, Source 3

Mississippi

- Over $250,000 in sales during any 12 calendar month period

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Missouri

- Over $100,000 in sales during a 12 month period ending any quarter (e.g. July 1, 2021 to June 30, 2022 or April 1, 2022 to March 31, 2023)

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: TPP only

- Source 1, Source 2

Montana

No sales tax

Nebraska

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: No

- Source

Nevada

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: No

- Source

New Hampshire

No sales tax

New Jersey

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: TPP, specified digital products, and taxable services only

- Source

New Mexico

- $100,000 in sales during the prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

New York

- Over $500,000 in sales AND 100 transactions during any 12 month period ending any quarter (e.g. July 1, 2021 to June 30, 2022 or April 1, 2022 to March 31, 2023)

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: TPP only

- Source

North Carolina

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

North Dakota

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: Taxable transactions only

- Source

Ohio

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: No

- Source

Oklahoma

- $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: Taxable transactions only

- Source

Oregon

No sales tax

Pennsylvania

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: Taxable transactions only

- Source

Puerto Rico

- Over $100,000 in sales OR 200 transactions during the seller’s accounting period

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Rhode Island

- $100,000 in sales OR 200 transactions during the prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: Nontaxable services excluded

- Source

South Carolina

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

South Dakota

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Tennessee

- $100,000 in sales during any 12 calendar month period

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: No

- Source 1, Source 2

Texas

- $500,000 in sales during any 12 calendar month period

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Utah

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Virginia

- Over $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: Yes

- Transactions made to a reseller excluded: Yes

- Limited to certain transaction types: No

- Source

Vermont

- $100,000 in sales OR 200 transactions during any 12 calendar month period

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Washington

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

West Virginia

- $100,000 in sales OR 200 transactions during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Wisconsin

- $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Wyoming

- Over $100,000 in sales during the current or prior calendar year

- Transactions made through a registered marketplace facilitator excluded: No

- Transactions made to a reseller excluded: No

- Limited to certain transaction types: No

- Source

Simplify Sales Tax with Fonoa

Streamline your sales tax processes with Fonoa. Our tax technology solutions simplify sales tax management for businesses selling in the United States. Stay compliant with state-specific requirements, track tax rates across 11,000+ jurisdictions, adapt quickly to changing tax laws, and effortlessly manage new products or business lines. Discover how Fonoa can help you navigate the complexities of sales tax. Contact us now to transform your tax operations.