France will mandate electronic invoicing (e-invoicing) and electronic reporting (e-reporting).

Detailed information on what this means in practice and how to comply is hard to find. The information published by the tax administration is helpful but often too technical for many tax practitioners. The information provided by law firms and tax technology providers is often remarkably high level and little more than marketing materials.

In this guide, we will explore the concept of e-invoicing in France, the requirements and mandates, and the steps businesses can take to comply with e-invoicing regulations.

Context of the Reform

In broad terms, what does the reform do?

Depending on the type of transaction, businesses will be required to either:

- Send an e-invoice to their customer using either a public government portal or directly through a certified intermediary platform called a “PDP”. This is known as e-invoicing.

- Send transactional information to the tax authority either directly to the public government portal or via a PDP. This is known as e-reporting.

Specific information must be provided in the context of both e-invoicing and e-reporting, which is discussed in more detail in subsequent parts of the guide.

The invoices must be produced in one of a small number of specific, structured formats. In practice, many taxpayers will rely on their PDP or an alternative invoice dematerialization business to ensure that invoices are submitted in the proper format.

The tax authority will use the invoice and e-reporting information to identify potential irregularities, non-compliance, and fraud.

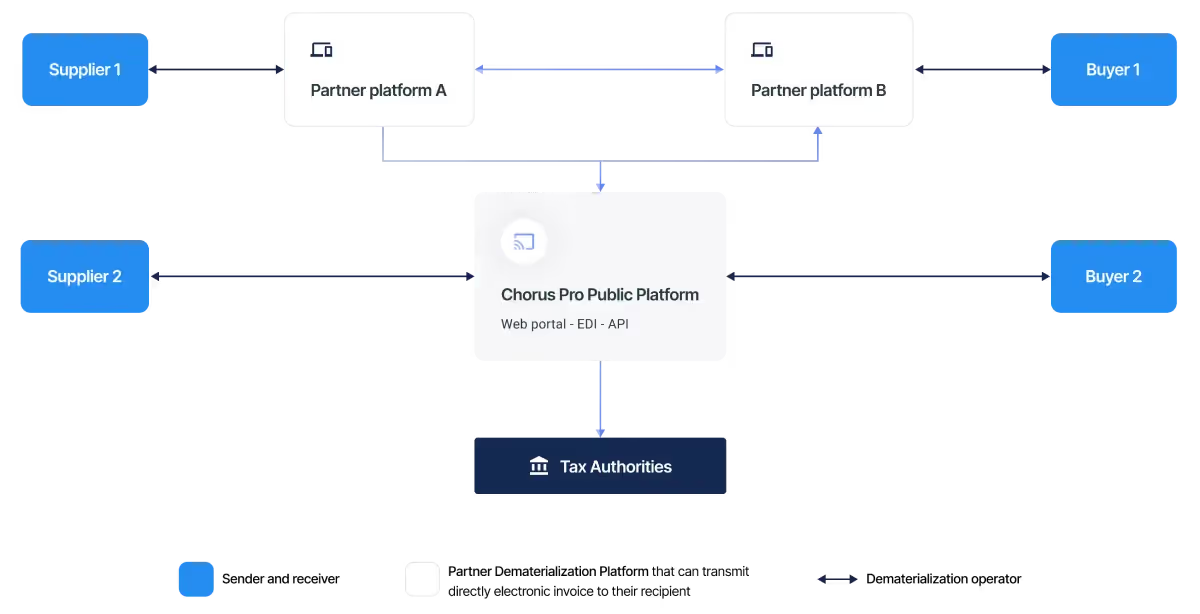

What is the Public Portal?

The public portal (PPF - “Portail Public de la Facturation”, or Public Invoicing Portal) offers a minimal base of services for exchanging invoices and concentrating the invoicing and e-reporting data for administration.

What is a PDP?

A PDP is a registered service provider offering dematerialization of invoices that can transmit electronic invoices directly to their recipients and transmit data to the public platform.

PDP stands for "Plateforme de Dématérialisation des factures à destination des Particuliers".

What is an OD?

An OD is an unregistered service provider offering dematerialization of invoices that can assist in the issuance or receipt of invoices, but is not able to transmit the invoices directly between the sender and the receiver. A taxpayer using an OD is therefore obligated to use the public portal as an intermediary.

"OD" stands for "Opérateur de Dématérialisation".

What is an e-invoice in French terms?

An e-invoice is an invoice that has been issued, transmitted and received in a structured data format, allowing for automatic and electronic processing.

A structured data format contains data without a visual representation, presented in a machine-readable format that can be ingested by an Account Payable (AP) system, eliminating the need for manual data entry. For example, e-invoices are not downloaded images of invoices such as JPG, HTML documents on a web page or in an email, or paper invoices sent electronically (e.g. faxes or scans of paper invoices)

E-invoices issued through the public portal must be issued in one of the 3 base formats compatible with the EN16931 standard: UBL, CII, and Factur-X. That means businesses using the public portal must either issue invoices in these formats directly from their invoicing system or use an OD to transform their non-compliant invoice into one of these formats.

Unlike ODs, PDPs can issue invoices directly to customers that also use a PDP without using the public platform. These invoices must be in a structured format but are not limited to one of the three invoicing formats described above. Therefore companies using a PDP can issue an invoice in a format that best suits their customer’s needs, provided that the PDP supports this format. Any reformatting operation performed by the PDP will have to ensure the maintenance of the integrity, authenticity, and completeness of the data.

What is e-reporting in France?

E-reporting is the transmission to the authorities of certain information (for example, the amount of the transaction, the amount of VAT invoiced, etc.) relating to commercial transactions not covered by e-invoicing (e.g. B2C transactions and cross-border transactions).

Unlike many other countries that have introduced e-reporting obligations, the French system requires reporting data concerning payment statuses.

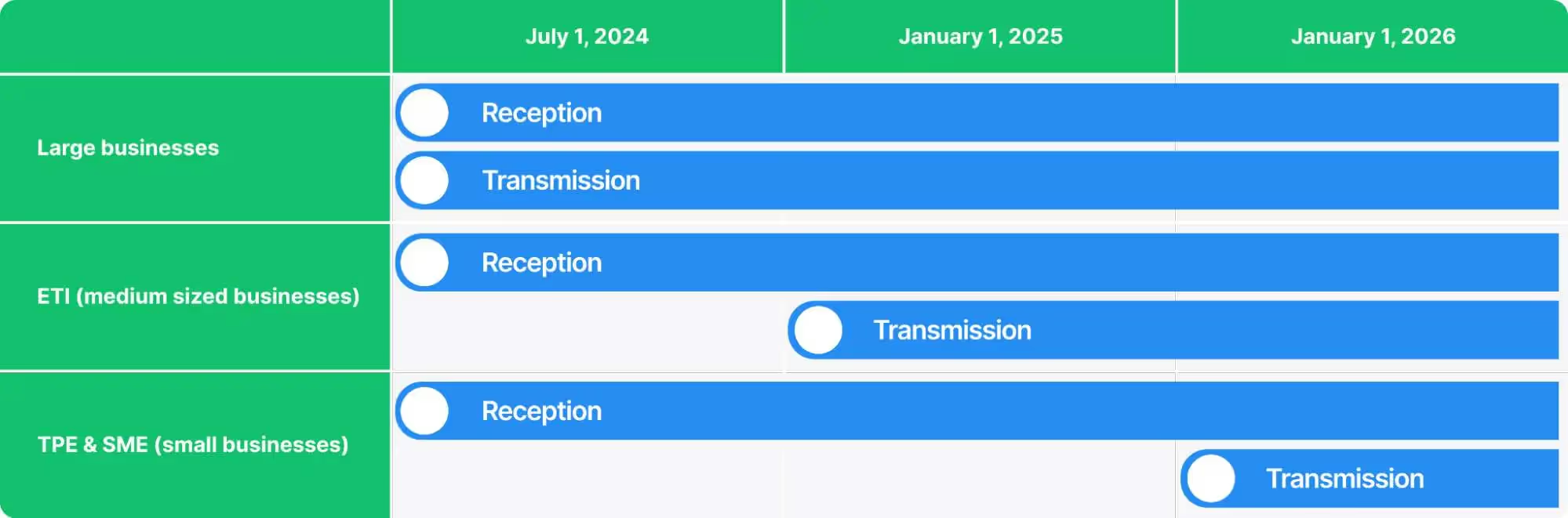

What is the timeline for the reform?

France has decided to postpone the implementation of the e-invoicing and e-reporting reform, which was initially planned to commence on July 1, 2024. The revised timeline for the rollout will be determined during the discussions for the Finance Law for 2024.

The implementation of electronic invoicing and the transmission of transaction data to the administration (e-reporting) was supposed to take place progressively according to the following initially announced timeline:

In summary, all businesses would need to be able to receive e-invoices by 1 July 2024. Large businesses would need to be able to transmit e-invoices and e-reporting information by 1 July 2024, medium-sized businesses by 1 January 2025, and small businesses by 1 January 2026. However, it's essential to note that the postponement may extend these dates further, as the exact revised dates are currently uncertain.

A large business is :

- Either a company employing more than 5,000 people, regardless of its annual sales or balance sheet total,

- Or a company with fewer than 5,000 employees, whose annual sales and balance sheet total exceed the thresholds of 1,500 million and 2,000 million, respectively.

An ETI, or a medium-sized business, is:

- A business that does not fall into the small business category,

- And has fewer than 5,000 employees AND annual sales not exceeding 1,500M€ euros or total assets not exceeding 2,000M€

TPEs and SMEs, or small businesses, are:

- Businesses with fewer than 250 employees,

- And have annual sales of less than 50 million euros or total assets of less than 43 million euros

How will the e-invoicing system work in France?

Which transactions are in the scope of the e-invoicing requirement?

E-invoicing applies to all purchases and sales of goods and/or services between companies established in France that are subject to French VAT.

Transactions exempt from VAT under articles 261 to 261 E of the French General Tax Code are not subject to electronic invoicing. These include:

- Healthcare services (article 261, 4, 1°)

- Education and training services (article 261, 4, 4°)

- Real estate transactions (article 261, 5),

- Transactions carried out by non-profit associations (article 261,7),

- Banking and financial transactions and insurance and reinsurance transactions (article 261C).

What information needs to be provided for e-invoicing?

Initially, twenty-four (24) items are mandatory. These items are listed in the External specifications file for electronic invoicing document published by the tax authorities (available in English and French).

An additional seven (7) invoice data fields will be required as of 1 January 2026 (or later):

- Price markdown (discounts and rebates)

- Detailed description of goods delivered or services rendered

- Quantity of goods delivered or services rendered

- Price exclusive of tax for each good delivered or service rendered

- Delivery address / address of performance of service, if different from customer’s address

- Date of issue of the rectified invoice in the event of an amended invoice

- Eco contribution amount.

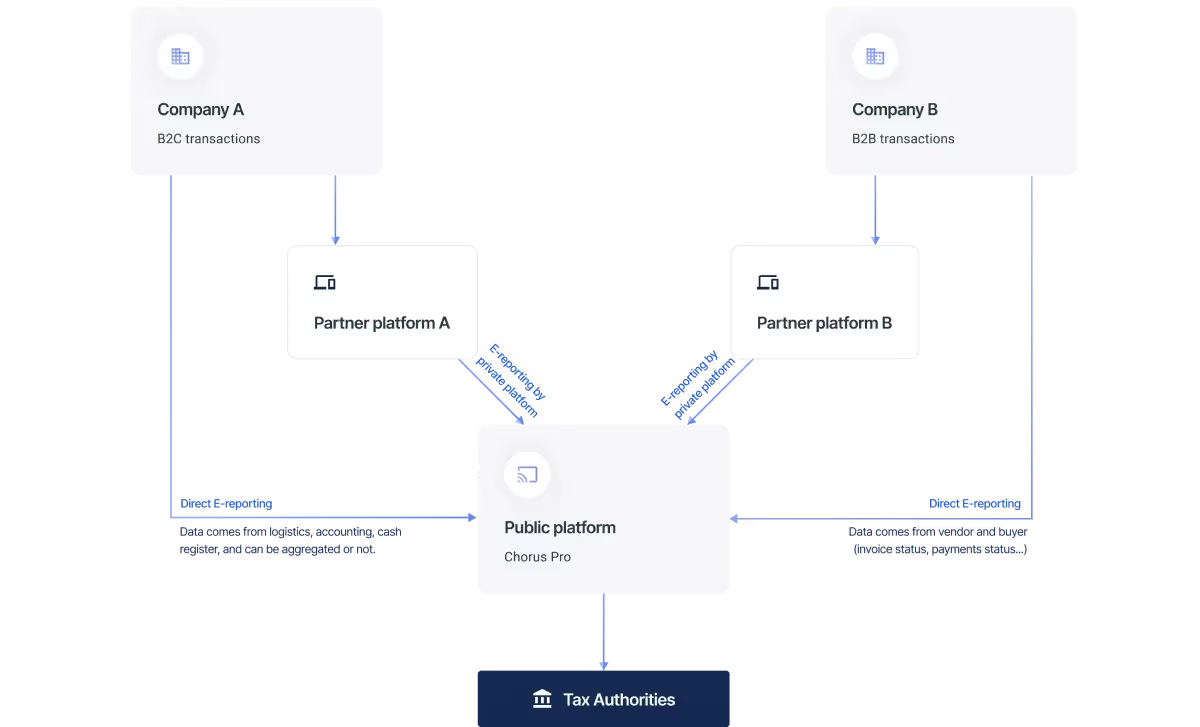

How does the e-invoicing process look in practice?

- Supplier produces an invoice: The supplier produces an from its ERP or invoicing system, which will generally not be in one of the structured invoicing formats accepted under the e-invoicing reform.

- Invoice is dematerialised into an accepted format: Assuming the supplier does not generate its invoices in one of the structured invoicing formats accepted under the e-invoicing reform, it will usually rely on either a PDP or a non-certified OD to convert their invoices to an appropriate format. Alternatively, an e-invoice can be created directly on the public platform.

- Buyer identified in the directory: In order to ensure the interoperability of the e-invoicing ecosystem, there will be a central directory managed by the public platform containing the information necessary to route invoices to companies and organizations. This directory will identify all French-established businesses and indicate whether they use a PDP or the public platform for e-invoicing.

- Invoice is sent either directly or indirectly to the buyer

- Once the buyer has been identified in the directory, the supplier or the supplier’s PDP will know what path the invoice should take.

- Direct

In the case of supplier 1, the PDP is in charge of sending the e-invoice. If the buyer also has a PDP, the seller can send an invoice directly to the buyer’s PDP without having to pass through the public platform. The invoice must be exchanged in a structured format, but it is not limited to one of the three formats used by the public platform (discussed in detail below).If the buyer does not have a PDP, the invoice is sent to the buyer via the public platform. One of the three prescribed invoicing formats must be used. - Indirect

In the case of supplier 2, the invoice is sent to the buyer via the public platform. The same directory will be used to identify the buyer and whether the buyer also uses the public platform or a PDP. One of the three prescribed invoicing formats must be used. If the buyer uses a PDP, the e-invoice will be routed directly to that PDP.

- Direct

- Once the buyer has been identified in the directory, the supplier or the supplier’s PDP will know what path the invoice should take.

- The buyer receives the invoice through the public platform or its PDP. If receiving through the public platform, it may need the services of an OD to reformat the invoice so that it can be ingested by its AP system.

Can my invoice be rejected?

Yes. A series of automated tests are performed either by the PDP or the public portal. If any of the tests fail, the invoice is rejected.

In broad terms, the checks can be categorized as follows:

- Technical checks: antivirus control, empty file control, signature control and verification, control of the uniqueness of the file name (to prevent duplicate invoices), etc.

- Application controls: syntax format analysis (ensuring that the invoice format is admissible)

- Functional controls: uniqueness of the information (to prevent duplicate invoices), data consistency checks, unknown recipient, etc.

- Business controls: data validity check by the recipient

Will more information be required on the invoices?

Yes. The following invoice data fields are new:

- the buyer’s SIREN number;

- the transaction type, e.g. goods or services

- the shipping address or address of where the service was rendered.

How will the e-reporting system work in France?

What operations are affected by e-reporting?

As a general rule, e-reporting obligations apply to taxable persons established in France on international transactions between taxable persons ("International B2B transactions") as well as transactions performed for a non-taxable person ("B2C").

Taxable persons not established in France but liable to collect French VAT will be subject to the e-reporting obligations unless they benefit from the OSS-IOSS scheme. This usually only relates to B2C transactions.

B2C transactions include the following:

- Domestic supplies of goods

- Intra-community distance sales of goods from France

- Distance selling from another EU member to France and subject to French VAT

- Supplies of services taxable in France to a non-VAT registered customer

International B2B transactions include the following:

- Intra-community deliveries of goods and services.

- Intra-community acquisitions.

- Exports made to companies outside of the EU.

- Operations destined for communities in overseas territories.

In addition, French e-reporting obligations can sometimes apply not to the seller but to the buyer, notably in the case of the reverse charge. The following transactions would normally subject the buyer to e-reporting obligations when the supply is taxable in France:

- Intra-community acquisitions

- Acquisition of goods in France that are subject to the domestic reverse charge

- Purchases of goods from Monaco

- Purchases of services deemed to be taxable in France from a non-established seller (e.g. services related to immovable property)

- Purchases of services from Monaco

In practice, many businesses with complex operations conduct transaction mapping exercises to better understand which of their business flows would be impacted by these requirements.

What information needs to be provided for e-reporting?

The data expected in the context of e-reporting differs depending on whether it concerns international B2B transactions or B2C transactions.

For international B2B transactions, the data to be transmitted will be identical to those transmitted in the context of e-invoicing, except for the unique identification number (SIREN) of the buyer.

For B2C transactions, far fewer data elements must be submitted.

A list of the information to be submitted is available in the “External specifications file for electronic invoicing” document published by the tax authorities (available in English and French). The link is available here.

In addition to transaction data, payment data will also have to be reported to the public portal. The payment data consists of the following information:

- The corresponding transmission period

- Invoice number (except for B2C transactions where there is no invoice)

- Collection date

- Currency

- The amount collected by tax rate.

Payment data will be required only for supplies of services (excluding operations giving rise to a reverse charge of the VAT and excluding operations for which the option for tax payment based on debits has been chosen). This requirement applies both to the transactions falling under the scope of the e-reporting as well as the e-invoicing rules.

How does the e-reporting process look in practice?

- Supplier sends transactional information:

- Company A is not required to send an invoice (B2C supply) but has the option. Company B is required to send an invoice (B2B supply) but the transaction is not within the scope of the French e-invoicing regulations.

- If using a PDP, companies A and B can issue an invoice normally, and the PDP will extract the relevant transactional information from the invoice. If no invoice is issued (e.g. in the case of B2C transactions) the PDP should be able to pull the required transactional information from other sources.

- The information is provided to the tax authorities:

- If using PDP, then the PDP will send the transactional information to the public platform.

- If the company does not use a PDP, then it must send the transactional information itself directly to the public platform. If the company issues an invoice in one of the three approved invoicing formats, the public portal can extract the relevant transactional information from the invoice. An OD can assist with reformatting the invoice or extracting the necessary data, but cannot link directly with the public platform.

How often must transactions be reported?

The reporting frequency depends on the tax regime a business is subject to.

For companies under the normal tax regime, e-reporting must be done three times a month, no later than 10 days after the reporting period. The reporting periods are the following:

- 1st to 10th of the month

- 11th to 20th of the month

- 21st to last day of the month

How Fonoa Can Help

Fonoa provides a comprehensive solution for global e-invoicing and e-reporting requirements, including in France.

Through our innovative platform, Fonoa offers a seamless plug-and-play solution that effortlessly empowers companies to achieve global tax compliance. Implementation can take as little as a few weeks with our easy-to-use unified API. We offer excellent customer service and are able to support you every step of the way.

Contact us for more information.

Additional Resources: