Türkiye was one of the first countries in the EMEA region to introduce e-invoicing as a solution to reducing its VAT gap. The country has a mature e-invoicing system in place. Over the years, more electronic documents have been introduced by the Turkish Revenue Administration (TRA), such as electronic delivery notes (electronic transport documents), e-tickets, e-ledger, e-tab, etc. Taxpayers must store electronic records in compliance with the local laws that mandate keeping them locally.

For a more structured summary of the requirements, you can visit Türkiye country page for e-invoicing.

How does the e-invoicing system work in Türkiye?

Before everything, taxpayers must be aware that there are two different types of e-invoices in Türkiye: E-fatura and e-arsiv invoices. Each of these invoices comes with its unique scope and compliance prerequisites.

- E-fatura is an invoice that suppliers must issue if the buyer of the invoice is registered in the e-fatura system. According to Turkish regulations, taxpayers must register in the e-fatura system if their annual revenue is above a certain threshold (3 million TL for 2022 income) or if they operate in specific sectors. If a buyer of the invoice is registered in the e-fatura system, the Supplier must issue an e-fatura invoice, and if the buyer is not registered, e-arsiv invoices must be given. E-fatura is used for most B2B transactions.

- E-arsiv is an invoice that suppliers must issue if the buyer is not registered in the e-fatura system. Requirements for submitting an e-arsiv invoice to the tax authority differ from e-fatura. Therefore, suppliers need to know whether their buyers are registered in the e-fatura system. Even though it is possible to issue e-arsiv invoices for B2B transactions, the most common use case is B2C transactions.

What are the businesses in the scope of e-fatura and e-arsiv?

Taxpayers must register for e-fatura:

- If their gross sales revenue for 2022 exceeded TRY 3 million

- If they operate in the e-commerce, real estate, motor vehicle, construction sectors or taxpayers, who carry out production, purchase sale, or leasing transactions and act as intermediaries, if their gross sales revenue for 2020 and 2021 exceeded TRY 1 million; and for 2022 exceeded TRY 500,000

- If they provide accommodation services as a form of investment or under a special license without a threshold

Taxpayers must register for e-arsiv

- If they are registered for e-fatura

- If they operate in specific sectors(intermediary services, digital ad services etc.) and

if after March 1, 2022:

- the total amount of the invoice issued to a non-taxable taxpayer exceeds TRY 5,000;

- the total amount of the invoice issued to a taxable person exceeds TRY 2,000

If your business is in scope, you can continue reading to understand the steps you must take to comply with the Turkish e-invoicing mandate.

What taxpayers must do as a part of onboarding?

Taxpayers required to implement e-invoicing must register in the e-fatura and/or e-arsiv fatura system. To register in these systems, taxpayers must obtain digital signature certificates. Using digital signatures, taxpayers can apply for registration in e-fatura and/or e-arsiv fatura systems to start issuing electronic invoices.

If a taxpayer is using a private integrator in Türkiye, they must authorize the service provider through signing an authorization request in the private integrator system.This request will be delivered to the TRA by the integrator.

What are the options for e-invoice submission to the tax authority platform?

After registering in the e-fatura or e-arsiv systems, taxpayers must be able to submit their invoices to the tax authority platform. There are three different ways to do so:

- Manual submission through web portal: This method is mainly adopted by small taxpayers with low volumes of invoices.

- Direct integration to the TRA platform through API: This method is adopted by large enterprises with IT teams and infrastructure.

- Private Integrator: Most taxpayers use a third-party service provider to submit their e-invoices to the TRA systems. Third-party service providers must be certified by the TRA. The certification is granted per document type (e-fatura, e-arsiv, e-delivery note, etc.). Taxpayers might use more than one private integrator.

E-invoice Format and E-invoicing steps

E-fatura and e-arsiv invoices must follow a structured UBL 2.1. There are different requirements concerning e-fatura and e-arsiv submission.

E-fatura invoices are subject to a clearance system. This means that e-fatura invoices require the TRA's approval to be considered valid. Therefore, suppliers must digitally sign and submit their e-fatura invoices to the TRA after generating the UBL file. The TRA system performs checks, and if the e-invoice has no errors, the TRA delivers it to the buyer. Therefore, suppliers do not need to submit e-fatura invoices to their buyers as the TRA system handles the delivery.

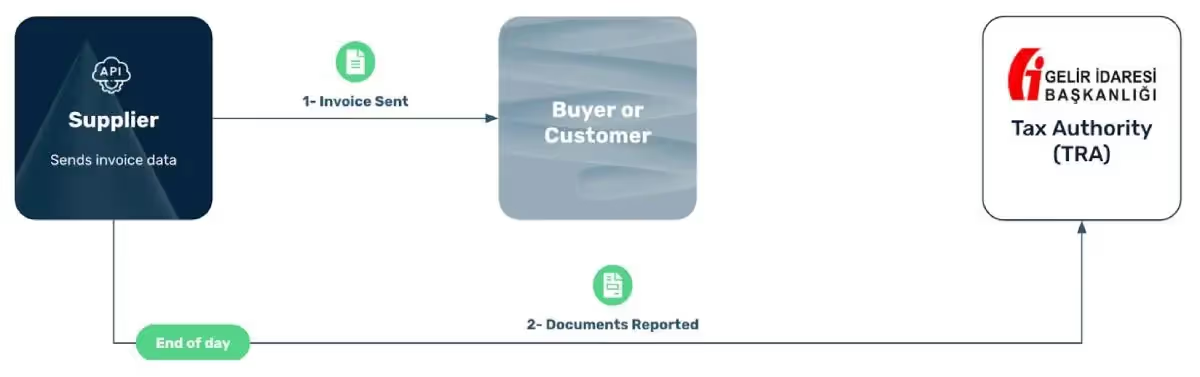

In the case of e-arsiv invoice, there is no clearance needed. E-arsiv invoices are delivered to the recipient/buyer first, and then within 24 hours, it is reported to the TRA. Therefore, the buyer of the invoice receives it from the Supplier.

E-fatura Flow

E-arsiv Flow

E-archiving

E-invoicing obligations often bring electronic storage requirements as electronic invoices have legal value and must be preserved without alteration during the storage period.

In Turkiye, e-invoices must be stored for ten years for fiscal evidence. The Turkish legislation requires original documents to be stored in Türkiye. Taxpayers may keep copies abroad. If outsourced to a third party, the TRA must certify the third-party service provider. There are other security measures applicable to electronic storage.

What is the difference between commercial and basic e-fatura?

E-fatura has two scenarios that businesses can decide with their counterparties and adopt.

The commercial e-fatura scenario allows recipients of the invoice to respond to the e-fatura they received by simply accepting or rejecting the invoice. Basic e-fatura does not allow e-fatura recipients to respond.

In a commercial scenario, the buyer's response goes to the TRA first, and then the Supplier of the invoice receives it through the status update from the TRA. Buyer rejection is used as a means to cancel the e-fatura invoice.

Basic Flow

Commercial Flow

What are the main challenges of the implementation of e-invoicing (e-fatura and e-arsiv) in Türkiye?

The Turkish e-invoicing system is complex as it requires a big orchestration for understanding the invoice type to issue, signing each document and storing e-invoices in a compliant manner.

- Determining the e-invoice type is quite challenging in Türkiye as the invoice issuer must know whether their buyer is registered in the e-fatura system. The TRA's website allows a manual search of the buyers' registration status for e-fatura and e-arsiv invoices. Some solution providers, like Fonoa, automated this process, allowing customers to check their buyer's registration status as a part of the e-invoice issuance process.

- E-invoice numbering can also be confusing, mainly when it's based on the document type being issued. If the document type is not determined correctly, issuing correctly sequenced invoices will not be managed accurately. Therefore, spotting the correct document type is paramount in the process.

- As part of the e-invoicing process, taxpayers are assigned a mailbox to receive e-invoices, called an alias. Taxpayers who have multiple branches or multiple private integrators might have more than one mailbox (alias). This means that suppliers must send invoices to the correct aliases. Sometimes, it is hard to get the right one as some of the mailboxes might need to be updated. Therefore, using a valid alias code is crucial to issue correct e-invoices.

- E-invoices must be digitally signed. Special integrator’s signatures can be used for this purpose. This means that digital signature operation can be outsourced to special integrator’s.

- Finally, storing original e-invoices locally in Türkiye might also present challenges to some international companies whose headquarters and storage locations are located abroad.

How can Fonoa help?

Fonoa e-invoicing provides a comprehensive and indispensable solution for businesses operating in Türkiye. Our tailored offering addresses the unique challenges of e-invoicing implementation in Türkiye. We excel in simplifying the process by automating essential tasks such as e-fatura/e-arsiv registration checks, sequential invoice number assignment, and ensuring accurate alias assignment. Moreover, we understand the importance of local compliance, so we facilitate the local storage of e-invoices within Türkiye. With Fonoa e-invoicing, you can trust that your business will meet regulatory requirements and operate efficiently and effectively in the Turkish market.