Czechia VAT Guide for International Businesses

VAT Rates in Czechia

The standard VAT rate (”Dan z pridane hodnoty” (DPH)) in the Czech Republic is 21%, with some services exempt from Czech VAT, such as postal services, financial services, and medical care.

VAT Registration Thresholds in Czechia

- VAT registration threshold for domestic established sellers: CZK 2 million (approximately EUR 84,000) turnover in the preceding 12 consecutive calendar months.

- As of January 1, 2025: VAT registration threshold for domestic established sellers: 2,000,000 (approximately EUR 80,000) turnover/ calendar year, for which the taxable person becomes CZ VAT payer from the first day of the following calendar year;

- VAT registration threshold for domestic established sellers: after the date on which its domestic turnover exceeded CZK 2 536 500 (approximately EUR 100,000) in the relevant calendar year.

- VAT registration threshold for non-established sellers: No registration threshold.

- VAT registration threshold for intra-EU distance selling of goods and B2C telecommunications, broadcasting & electronic services (TBE): EUR 10,000 (net) per calendar year.

- VAT registration threshold for non-resident, non-EU-based suppliers of Electronically Supplied Services (ESS): No registration threshold.

Czech VAT Number Format

Czechia uses TIN-like numbers (Personal Numbers) (”Rodné cislo”) for identifying its taxpayers.

- For individuals, the Personal Number consists of:

- 9 digits, if the person was born before January 1, 1954

- 10 digits, if the person was born after January 1, 1954

- For businesses, the Tax Identification Number (TIN) consists of 8 digits

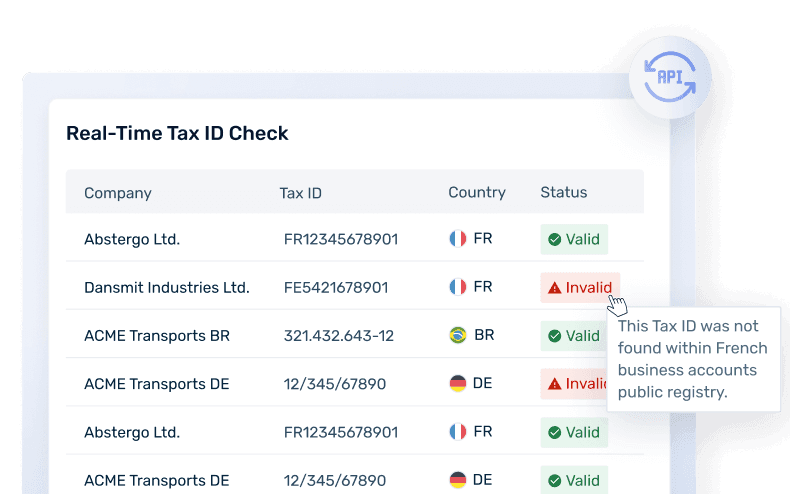

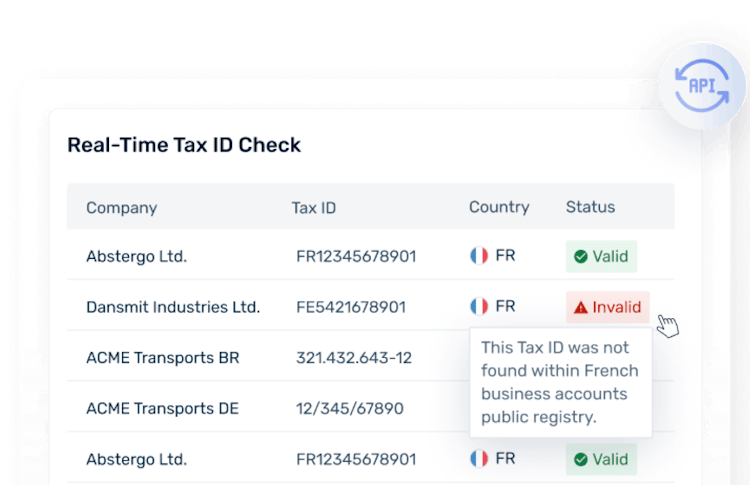

The VAT ID structure for VAT-registered taxpayers changed with Czechia EU accession. The tax identification number comprises the code of the country “CZ” and core part of the existing TIN (i.e. in most cases it is a birth number of a natural person or company ID = IČO in the case of the legal entity). That means that the code “CZ” is at the beginning instead of the existing code of the tax administrator, in practice, the first three digits and the hyphen are replaced by the code "CZ".

- New format: CZ then 8 to 10 digits ranging from 0 to 9.

- For individualsFormat: 999999/9999

- For businessesFormat: 99999999

VAT on Electronically Supplied Services (ESS) in Czechia

Digital Services in the European Union (EU) are often referred to as electronically supplied services (ESS). Czechia applies the harmonized EU VAT rules for ESS.

- For B2B supplies of such services, the general place of supply rule for services has to be taken into consideration.

- For B2C supplies**,** the EU ESS rules should apply to foreign companies selling to Czech consumers.

Under the EU’s B2C ESS rules, until the sales value reaches EUR 10,000 (including distance sales of goods), the seller can charge VAT where it is resident. Once the sales exceed the threshold, the seller should register for VAT in the Czech Republic, or it can choose to account for the VAT under the EU’s One Stop Shop (OSS) regime.

VAT Rate: 21% VAT is typically applied to the sale of affected Electronically Supplied Services.

Will your business need to pay VAT on digital services in Czechia in 2024?

Learn More About VAT on Digital Services in Czechia

Marketplace & Platform Operator Rules in Czechia

Czechia applies the harmonized European Union’s (EU) VAT rules for marketplace & platform operators.

Supply of goods

A marketplace is deemed to have received and supplied the goods themselves. This transaction is split into two supplies:

- A supply from the underlying supplier to the marketplace (deemed B2B supply)

- A supply from the marketplace to the final customer (deemed B2C supply).

This rule covers the following:

- Distance sales of goods imported to the EU with a value not exceeding EUR 150

- Supplies of goods to customers in the EU, irrespective of their value, when the underlying supplier is not established in the EU (both domestic supplies and distance sales within the EU are covered).

Supply of services

When electronically supplied services are sold through an intermediary, e.g. a marketplace for applications, the intermediary is deemed to have received and supplied the services themselves. Therefore, the VAT liability shifts to the intermediary from the underlying supplier.

Invoice Requirements in Czechia

According to the Czech VAT Act, invoices should contain the following data:

- Document & general transaction information

- Invoice number

- Issuance date

- Delivery date or the date of receipt of an advance payment if this date is prior to the invoice issue date

- Supplier information

- Name, address, and tax identification number

- Customer information

- Name, address, and tax identification number

- Financial transaction information

- Quantity and description or type of the goods delivered or services performed

- Unit price without VAT and discount, if not included in the unit price

- VAT base

- VAT rate

- Amount of VAT (in CZK)

- Additional information that may be required:

- Reference to VAT exemption

- Reference to self-billing

- Reference to reverse charge mechanism

- Reference to any special scheme

A simplified invoice may be issued if the total amount does not exceed CZK 10,000 and should contain the following information:

- Supplier data: name, address, tax identification number;

- Invoice number and issuance date;

- Delivery date or the date of receipt of an advance payment if this date is prior to the invoice issue date;

- Quantity and description or type of the goods delivered or services performed;

- VAT rate;

- Total amount of the invoice.

E-Invoicing & Digital Reporting for Czechia

E-invoicing is permitted in Czechia but is not mandatory.

The Czech Republic intended to introduce the electronic registration of sales revenues (ERS) in 2019. Businesses subject to Czech income tax from certain sectors (hotel, restaurant services, wholesale and retail sector), would have had real-time reporting obligations in relation to their domestic supplies if the payment was made in cash, vouchers, gift cards, and the like. Bank transfers, credit, and debit card payments were out of scope. In 2022, the Czech government abolished the requirement effective January 2023, due to the decreasing amount of cash transactions. Thus, there is currently no mandatory digital reporting obligation in effect in Czechia. Taxpayers will be able to report their sales data on a voluntary basis until December 31, 2023.

Though there is no mandatory obligation in place, electronic invoices issued for B2G transactions should be accepted where they are in a format compatible with the European standard for e-invoicing. Contracting authorities should not be able to reject an e-invoice when in this format.

Learn more about E-Invoicing and Digital Reporting in Czechia

Governmental Body Responsible for E-invoicing and Digital Reporting in Czechia

The governmental body responsible for e-invoicing and tax matters in Czechia is the Financial Administration (”Finanční Správa” (FS)).

VAT Payments and Returns in Czechia

Full VAT Returns

Penalties in case of late filings or misdeclarations

In the case of the late filing of VAT returns and payments, the Czech Tax Authority should enforce the following penalties:

- For late submission of the VAT return, a penalty of 0.05% of VAT due for each day of the delay may be imposed. However, the penalty cannot be higher than 5% of the VAT due or a maximum of CZK 300,000 (approximately EUR 12,500) per VAT return. The penalty could be imposed from the sixth working day of the delay (the first five working days are penalty-free).

- For VAT underpayment, a penalty of 20% of the additionally assessed VAT may be imposed on the taxpayer.

- In case the taxpayer fails to file VAT returns electronically, a penalty of CZK 1,000 (approximately EUR 40) may be imposed.

- For late payment of VAT, taxpayers may pay late payment interest, which is calculated as a rate declared by the Czech National Bank, plus 8 percentage points.

Fonoa does not provide professional tax opinions or tax management advice specific to the facts and circumstances of your business and that your use of the Specification, Site, and In addition, due to rapidly changing tax rates and regulations that require interpretation by your qualified tax professionals, you bear full responsibility to determine the applicability of the output generated by the Specification and Services and to confirm its accuracy. No professional tax opinion and advice. Fonoa does not provide professional tax opinions or tax management advice specific to the facts and circumstances of your business and that your use of the Specification, Site, and In addition, due to rapidly changing tax rates and regulations that require interpretation by your qualified tax professionals, you bear full responsibility to determine the applicability of the output generated by the Specification and Services and to confirm its accuracy.