Türkiye VAT Guide for International Businesses

VAT Rates in Türkiye

The standard VAT rate (”Katma Değer Vergisi” (KDV)) in Turkey is 20%, with some services exempt from Turkish VAT, such as financial transactions, leasing immovable property by individuals, and water for agriculture.

VAT Registration Thresholds in Türkiye

- VAT registration threshold for domestic established sellers: No threshold

- VAT registration threshold for non-established sellers: No threshold

- VAT registration threshold for non-resident suppliers of Digital Services to non-taxable entities (B2C): No threshold

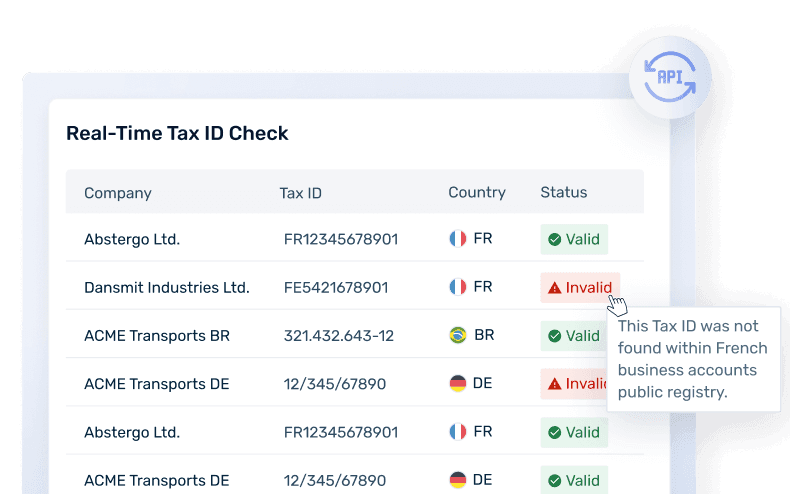

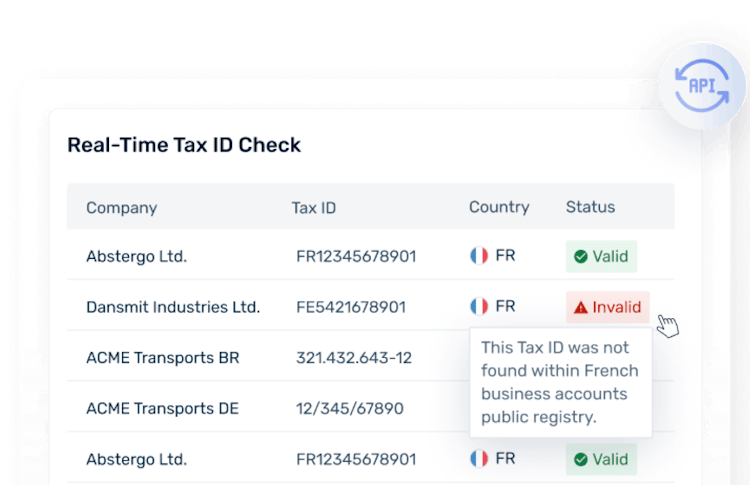

Turkish VAT Number Format

In Turkey, all legal entities, unincorporated entities, and individuals should have a tax identification number (TIN) (”Vergi Kimlik Numarası” (VKN)).

- Individuals: an 11-digit National Identity Number (”Türkiye Cumhuriyeti Kimlik Numarası” (T.C. Kimlik No.)) is used as the unique identification number. The TIN is matched with their National Identification Number.

- For foreign individuals who are staying in Turkey for longer than 6 months, it should be mandatory to obtain a TIN. Foreigners’ TIN consists of 10 digits, but they are allowed to use their Foreign Identity Numbers, if available.

- Format: 9999999999

- Businesses: the TIN number consists of 10 digits and it is obtained automatically or via registering with local tax offices. Digits can be any number between 0 and 9. If the company name starts with A, the first digit is 0; if starts with B, it is 1; if it starts with Y or Z it is 9, hence fort.

- For individualsFormat: 99999999999

- For businessesFormat: 9999999999

VAT on Digital Services in Türkiye

Non-resident taxpayers supplying digital services (also known as Electronically Supplied Services (ESS)) to non-taxable entities in Türkiye (B2C) should be subject to VAT in Türkiye. The ESS provision has been in place since 2018. This is not to be confused with Digital Services Taxes (DST) which is an entirely different tax.

VAT Rate: 20% VAT is applied to the sale of affected digital services. However, in case a service is subject to a reduced rate in Turkey, the reduced rate should be applied.

Taxable digital services in Türkiye

The Turkish VAT Act and related final communique do not define digital services. However, practically speaking, the following services should qualify as digital services in Türkiye:

- Streaming video, music, or online gaming;

- E-books;

- Hosting websites;

- Services related to mail, telephone, telegrams, telex, radio, and television.

Will your business need to pay VAT on digital services in Türkiye in 2024?

Learn More About VAT on Digital Services in Türkiye

Marketplace & Platform Operator Rules in Türkiye

Türkiye has not introduced special VAT obligations on Marketplace and Platform Operators.

Invoice Requirements in Türkiye

Tax invoices should contain the following information:

- Document & general transaction information

- Date of issuance

- Delivery date

- The sequence number of the invoice

- Supplier information

- Name, business address, and the TIN

- Customer information

- Name, business address, and the TIN

- Financial transaction information

- A description sufficient to identify the goods or services supplied, the quantity, and the price

- Additional information that may be required

- Waybill number

E-Invoicing & Digital Reporting for Türkiye

In Türkiye, two different e-invoice types exist.

- Türkiye requires use of an e-invoice application (”e-Fatura”) for B2B and B2G transactions for specific sectors and for medium and large taxpayers, a clearance e-invoicing obligation with the Turkish Revenue Administration. This requirement has been in place since 2012.

- In 2013 Türkiye introduced the e-arsiv (”e-Arşiv”) invoice requirement for all B2C and some (smaller) B2B transactions. E-arsiv is classified as a quasi-real-time reporting system.

Since 2012, Türkiye has continuously expanded the scope of e-invoicing and digital reporting obligations.

Learn more about E-Invoicing and Digital Reporting in Türkiye

Governmental Body Responsible for E-invoicing and Digital Reporting in Türkiye

The governmental body responsible for e-invoicing and digital reporting in Turkey is the Directorate of Revenue Administration of the Ministry of Finance (”Gelir İdaresi Başkanlığı” (GIB)).

VAT Payments and Returns in Türkiye

Full VAT Returns

Turkey has a special VAT return for non-resident taxpayers supplying qualifying digital services.

For more information, see a VAT on Digital Services Guide.

Penalties in case of late filings or misdeclarations

In the case of the late filing of VAT returns and payments, the Turkish Tax Authority should enforce the following penalties:

- Late filing of tax declarations should be subject to an irregularity penalty and tax loss penalty.

- Irregularity is the failure to comply with the formal and procedural provisions of tax laws and is punished according to the degrees written in the Turkish Tax Procedure Act. Late filing qualifies as a first-degree irregularity and a lump-sum penalty may be imposed, the amount changes per year. If the irregularity requires ex officio consideration, the penalties may be doubled.

- The tax loss penalty is the amount of the tax itself.

- In case of non-compliance with the obligation to submit an electronic declaration, a special irregularity penalty might be imposed.

- Late payment interest is calculated on the late payment of taxes due.

Fonoa does not provide professional tax opinions or tax management advice specific to the facts and circumstances of your business and that your use of the Specification, Site, and In addition, due to rapidly changing tax rates and regulations that require interpretation by your qualified tax professionals, you bear full responsibility to determine the applicability of the output generated by the Specification and Services and to confirm its accuracy. No professional tax opinion and advice. Fonoa does not provide professional tax opinions or tax management advice specific to the facts and circumstances of your business and that your use of the Specification, Site, and In addition, due to rapidly changing tax rates and regulations that require interpretation by your qualified tax professionals, you bear full responsibility to determine the applicability of the output generated by the Specification and Services and to confirm its accuracy.