Part of the SYNAPSE 2026 series | Keynote | Rob van der Woude, CTO, Fonoa

Why tax infrastructure built for the past is starting to break

Most tax operations look solid until they are put under pressure. Then the spreadsheets slow down, the batch jobs start failing, and the processes that held everything together at one scale stop working at the next.

This is typically because tax infrastructure hasn’t been built for what the business became, or for the compliance environment that has developed around it.

This is the challenge Rob van der Woude, Chief Tax Officer of Fonoa, put to the room in his opening keynote at SYNAPSE 2026, Fonoa's annual conference for indirect tax professionals.

The Path to No-Touch Tax opened with a question: how many of the foundations holding your tax operations together were built for a world that no longer exists?

Keep reading for three key insights from the rest of the session.

1. The pressure is already building. Most businesses just haven't felt it yet.

Rob opened with something that reframes how to think about compliance risk. In an earthquake, the pressure builds long before anything breaks. The ground feels stable. Nothing looks different. But the forces accumulating underneath are moving in one direction, and at some point, the surface has to respond.

That is exactly where tax is right now.

In tax, we're sitting on top of a fault line." — Rob van der Woude, CEO, Fonoa

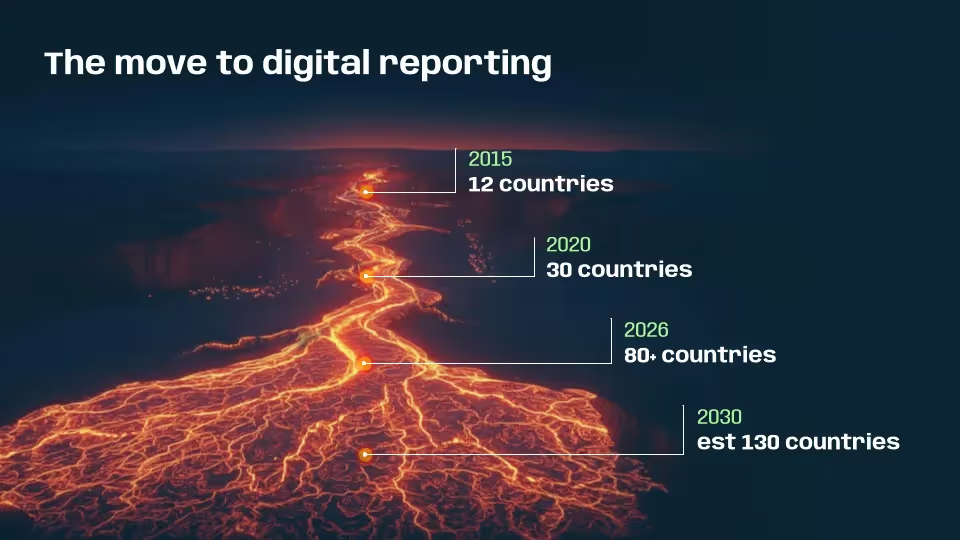

The evidence is in the numbers. In 2015, 12 countries had digital reporting requirements. By 2020, that was 30. Today it is over 80. By 2030, the estimate is 130.

That is not gradual change. That is exponential pressure, and 2030 is closer than most transformation timelines allow for. The businesses that feel fine right now are not necessarily safe. They are just yet to feel the ground move.

2. Why most tax infrastructure is one spreadsheet away from breaking

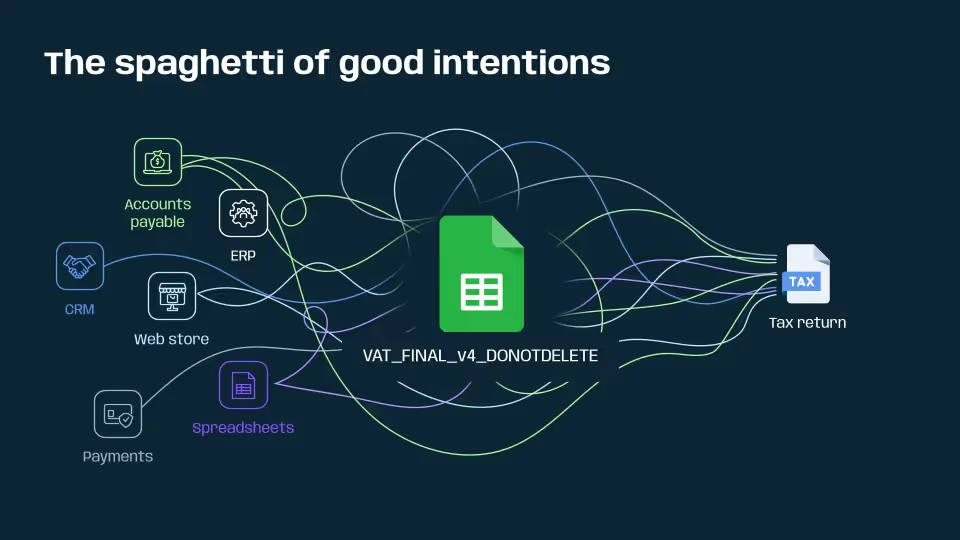

Rob named the problem with a phrase that resonated with everyone in the room immediately: the spaghetti of good intentions.

The diagram tells the story better than any description. Data flows in from CRM, ERP, accounts payable, web store, payments, and spreadsheets, tangling together into a single Google Sheet, one that has probably been renamed four times and carries the filename nobody is allowed to touch. That file produces the tax return. Every connection in that diagram made sense when it was built. Collectively, they have created something fragile, unscalable, and genuinely difficult to audit.

Tax mandates are expanding. Real-time reporting is becoming standard in more markets every year. The compliance environment is accelerating faster than most businesses anticipated, and the systems that handled it five years ago are already struggling to keep pace.

3. Weak foundations, not external forces, determine the outcome

Rob's earthquake metaphor reframes how to think about compliance risk.

When a mandate changes or a new reporting requirement arrives, it can feel like an external force the business simply has to absorb. But whether that change causes serious disruption or gets handled cleanly comes down to what was already in place before it arrived.

The mandate changes, the authority scrutiny, the new e-invoicing requirements: those make up the earthquake. The batch reconciliation process, the siloed tax team, the spreadsheet with four versions of the same filename: those are the foundation. One is outside your control. The other is not.

4. The goal is tax as a real-time, continuous process

The path Rob set out is not about buying better tools and layering them on top of the existing spaghetti. It is about rethinking what tax infrastructure is supposed to do. Compliance should not be something that happens at the end of a workflow, after the data has passed through six systems and a spreadsheet called DONOTDELETE. It should be embedded throughout, running continuously, catching issues as they arise, and operating the same way on a Tuesday in February as it does at month-end.

That shift, from periodic to continuous, from reactive to always-on, was the frame for every session that followed at SYNAPSE. The technology to support it exists. The obstacle, for most organisations, is the foundation work that has to happen first.

Bottom line: no-touch tax is a foundations problem, not a technology problem

The destination Rob described—a tax function that runs without manual intervention across every market a business operates in—is achievable. But it requires getting the foundations right first: clean data, continuous processes, and cross-functional ownership of compliance that does not sit with one team and one spreadsheet. Most organisations are not there yet. The good news, as Rob put it, is that the mechanism for getting there is familiar. The work is in starting it.

FAQs about no-touch tax

What is no-touch tax?

No-touch tax refers to a tax operating model where tax determination, reporting, and compliance processes run automatically without manual intervention. Instead of relying on spreadsheets and periodic reconciliation, tax is embedded directly into business systems and workflows, allowing compliance to happen continuously and in real time.

Why are tax authorities moving toward real-time reporting?

Tax authorities are increasingly adopting real-time or near real-time reporting to improve transparency, reduce fraud, and close the tax gap. Digital reporting requirements, e-invoicing mandates, and transaction-level reporting allow authorities to monitor tax data continuously rather than waiting for periodic filings.

What challenges prevent organisations from achieving no-touch tax?

Most organisations struggle with fragmented tax infrastructure. Data often flows across multiple systems—such as ERP, CRM, payment platforms, and spreadsheets—creating manual processes that are difficult to scale, audit, or automate. These disconnected systems make it difficult to implement continuous tax compliance.

Why are spreadsheets still common in tax operations?

Spreadsheets are often used because they are flexible and easy to implement when processes are first created. Over time, however, these spreadsheets become critical infrastructure that connects multiple systems. As reporting requirements grow and transaction volumes increase, these manual processes become fragile and difficult to maintain.

What is digital tax reporting?

Digital tax reporting refers to compliance systems where tax authorities require businesses to submit transaction-level tax data electronically, often in real time or near real time. Examples include e-invoicing mandates, continuous transaction controls (CTC), and digital VAT reporting systems.

How can businesses prepare for real-time tax compliance?

Preparing for real-time tax compliance typically requires improving data quality, integrating tax logic into core systems, and reducing reliance on manual reconciliation processes. Businesses also need tax infrastructure that can handle automated validation, reporting, and regulatory changes across multiple jurisdictions.

What role does tax infrastructure play in automation?

Tax infrastructure forms the foundation for automation. Clean data, integrated systems, and continuous processes enable tax determination and reporting to run automatically. Without strong infrastructure, automation tools cannot operate reliably.

Is no-touch tax achievable for global businesses?

Yes, but it requires a shift from reactive tax processes to embedded compliance. Organisations need systems that can operate across markets, adapt to changing mandates, and process tax data continuously. Many businesses are still early in this transition, but the technology required to support it already exists.

Why is tax compliance becoming more complex globally?

Tax compliance is becoming more complex because governments are introducing digital reporting mandates, e-invoicing systems, and real-time compliance requirements across more jurisdictions. The number of countries with digital reporting obligations continues to grow rapidly, increasing the operational pressure on tax teams.

.webp)