France's e-invoicing reform doesn't rely on a single central system. Instead, it distributes responsibility across a network of accredited platforms, a public portal, and a shared directory.

In our previous post, we explored the objectives and the scope of the French e-invoicing reform. We now turn to the structural foundation that makes the reform operational in practice: its architecture and the actors involved.

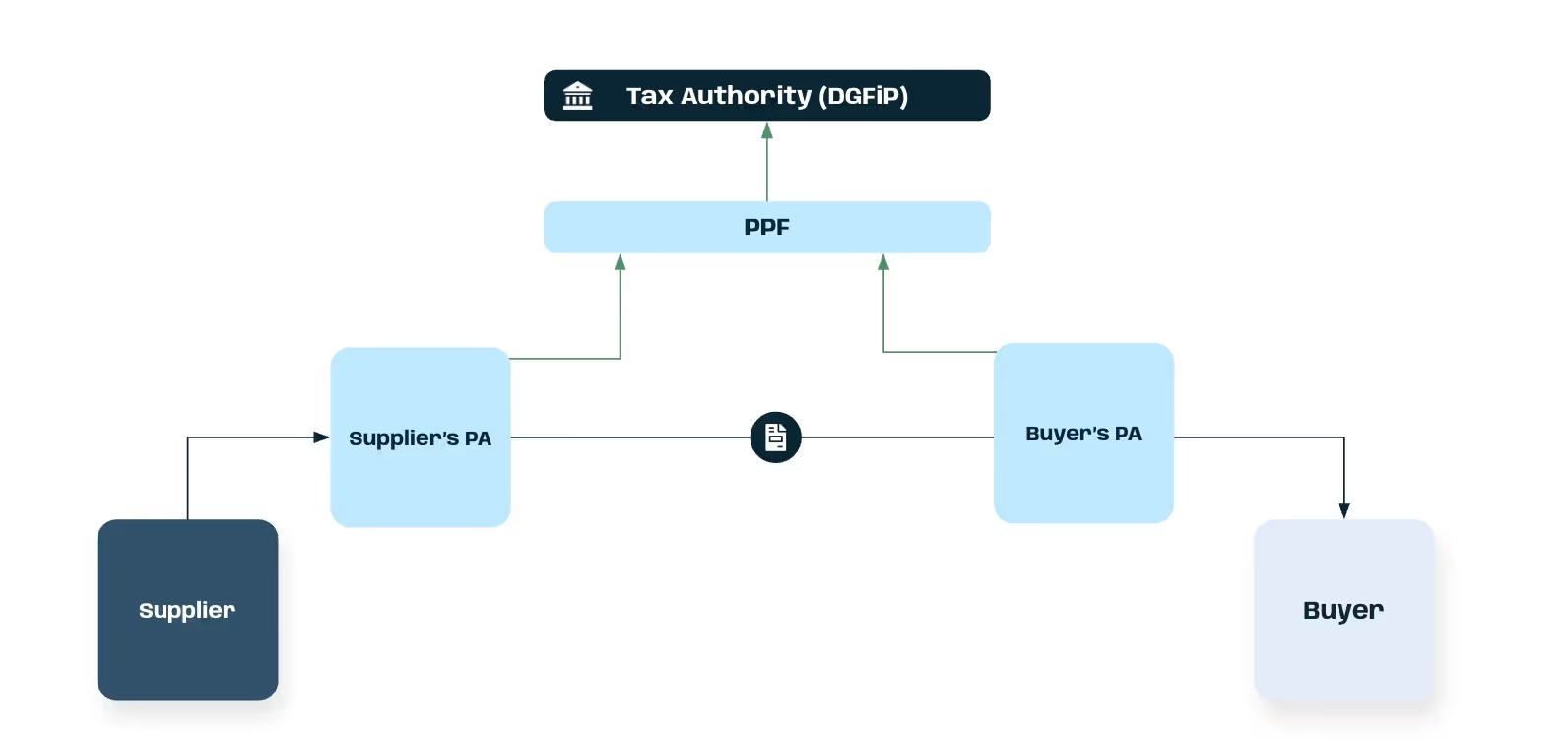

At the heart of the French model lies what is commonly referred to as the “5-corner model” or “Y-model”. Rather than relying on a single central exchange channel, France has adopted a decentralised framework built on interoperability between private Accredited Platforms and the Public Invoice Portal.

This architecture defines how invoices and regulatory data circulate, how platforms interact with one another, and how the tax administration receives the information required for compliance purposes.

What is the French 5-corner model?

The French 5-corner model, also referred to as the "Y-shaped model", describes the architecture used to exchange electronic invoices under the French e-invoicing reform. It involves five interacting participants:

- The supplier issuing the invoice

- The supplier’s Accredited Platform (PA-e)

- The buyer’s Accredited Platform (PA-r)

- The buyer receiving the invoice

- The Public Invoice Portal (PPF)

Invoices are exchanged directly between the accredited platforms (PA-e and PA-r). In parallel, the platforms transmit the required invoice data, transaction data, payment data, and lifecycle statuses to the Public Invoice Portal (PPF), which acts as a regulatory hub that centralises this information and forwards it to the tax administration.

The key actors of the French e-invoicing reform

Accredited Platforms (PA)

Accredited Platforms (PAs) sit at the centre of the French ecosystem. They are the only entities authorised to:

- Exchange domestic B2B electronic invoices.

- Transmit mandatory invoice data to the administration.

- Manage lifecycle statuses.

- Perform e-reporting transmissions.

Every in-scope business must appoint at least one PA.

Public Invoice Portal (PPF)

The Public Invoicing Portal (PPF) does not act as a platform for exchanging invoices between businesses (this function is handled exclusively by PAs). Instead, its role is centred on two primary functions:

- Maintaining the Central Directory (Annuaire) of VAT-registered businesses and their active electronic invoicing addresses, which enables correct invoice routing.

- Acting as a data concentrator, receiving invoice data, transaction data, and payment data from PAs and making this information available to the tax administration.

The PPF therefore operates as a regulatory hub rather than as a commercial exchange platform.

Compatible Solutions (SC)

Compatible Solutions (SC)Compatible Solutions (SC), such as ERP systems, billing software, or accounting tools, operate upstream or downstream of PAs. They assist businesses with invoice creation, data structuring, and integration into accounting systems.

However, they are not PAs. As such, they cannot exchange invoices within the regulated network or connect directly to the PPF. To participate in the French e-invoicing and e-reporting ecosystem, they must operate through a PA.

Connectivity and interoperability

Under the French mandate, businesses do not connect directly to the PPF. Instead, they integrate their ERP or billing systems with their chosen PA, which manages communication with the state infrastructure.

PAs are required to ensure interoperability for the exchange of e-invoices. The reform is structured around the Peppol interoperability framework, which provides the standardised technical infrastructure for platform-to-platform communication.

Interoperability ensures that any business can exchange invoices with any other business, regardless of which PA each party has selected. While Peppol accreditation is not explicitly mandated in the legislation, the interoperability requirements effectively mean that platforms must support standardised exchange mechanisms in order to operate at scale within the ecosystem.

The Central Directory (Annuaire)

At the heart of the architecture lies the Central Directory (Annuaire).

The Directory is a centralised registry that lists the electronic invoicing addresses of all VAT-subject businesses falling within the scope of the French e-invoicing reform. It provides the essential routing data required to deliver electronic invoices to a recipient’s chosen PA.

An electronic address is to an electronic invoice what a postal address is to a paper invoice: it precisely identifies the destination within the regulated network. The address follows a structured format: SchemeID:Identifier.

For domestic B2B e-invoicing in France, the recipient’s electronic address must use the scheme ID 0225.

In practice, this takes one of four mandated forms:

- 0225:SIREN: Identifies the legal entity as a whole.

- 0225:SIREN_SIRET: Enables routing at the establishment level.

- 0225:SIREN_SIRET_CODEROUTAGE: Enables routing to a specific service, department, or analytical code within a specific establishment (e.g., "Service A" or "Accounting").

- 0225:SIREN_SUFFIXE: Allows businesses to define multiple distinct addresses (for example, to separate purchasing channels) without linking them to physical establishments.

Each unique electronic address may be associated with only one receiving PA at any given time.

To guarantee end-to-end traceability, every electronic invoice must include:

- The recipient’s electronic address (for correct delivery).

- The issuer’s electronic address (to ensure lifecycle status messages, such as rejections, refusals, or payment confirmations, are routed back correctly).

Electronic invoicing addresses intended for receiving invoices are listed in the Central Directory. They can be queried by PAs and are also viewable via the PPF portal interface.

Frequently asked questions about the French e-invoicing architecture

What role do Accredited Platforms (PA) play in the French e-invoicing system?

Accredited Platforms (PA) are the central actors in the French e-invoicing ecosystem. They exchange electronic invoices between businesses, transmit mandatory invoice data to the tax administration, manage invoice lifecycle statuses, and perform e-reporting transmissions required under the reform.

What is the Public Invoice Portal (PPF)?

The Public Invoice Portal (PPF) is the government infrastructure that receives invoice and transaction data from Accredited Platforms. It maintains the Central Directory of electronic invoicing addresses and acts as a regulatory hub, making the transmitted data available to the French tax administration.

What is the Central Directory (Annuaire) in the French e-invoicing system?

The Central Directory (Annuaire) is a registry administered by the PPF that contains the identification data, electronic invoicing addresses, and routing information required to exchange electronic invoices within the French e-invoicing system. It lists all private businesses subject to VAT in France, as well as public entities (whether subject to VAT or not), and links their identifiers (such as SIREN or SIRET numbers) to their designated receiving PA.

The directory acts as a central routing hub, enabling PAs to identify the correct destination platform and route electronic invoices and related messages to the appropriate recipient.

How do businesses connect to the French e-invoicing system?

Businesses do not connect directly to the PPF Instead, they integrate their ERP, billing, or accounting systems with a PA, which manages invoice exchange and reporting obligations within the regulated network.

.webp)