In the previous posts, we explored the architecture of the reform and the key actors involved. We will now turn to the operational “flows” that make the system work in practice.

Under the French reform, all exchanges between Accredited Platforms (PAs) and the Public Invoice Portal (PPF) are structured into predefined transmission channels referred to as “flows.” Each flow corresponds to a specific type of data exchange. For example, one flow is used to transmit regulatory invoice data to the tax administration, another to route invoices between platforms, and another to communicate lifecycle status messages.

As discussed, the reform consists of two core components: e-invoicing and e-reporting. In this article, we focus on the e-invoicing component and the mandatory transmission flows that businesses must implement for domestic B2B transactions.

Types of invoices covered under French e-invoicing

Within the framework of electronic B2B domestic invoicing, several types of invoices are taken into account:

- Standard invoices

- Down payment invoices (factures d'acompte)

- Self-billing (auto-facturation)

- Factoring invoices (affacturage)

Corrections are handled through credit notes (avoir) or rectificative invoices (facture rectificative). These documents must reference the original initial invoice number and generate new lifecycle events

The journey of an invoice in the French e-invoicing system

The process begins with invoice creation. Under the French reform, invoices must be issued in a structured electronic format and transmitted through an Accredited Platform (Plateforme Agréée – PA).

The reform allows three formats:

- UBL (Universal Business Language)

- CII (Cross Industry Invoice / UN/CEFACT)

- Factur-X, a hybrid format combining a human-readable PDF with embedded structured XML data.

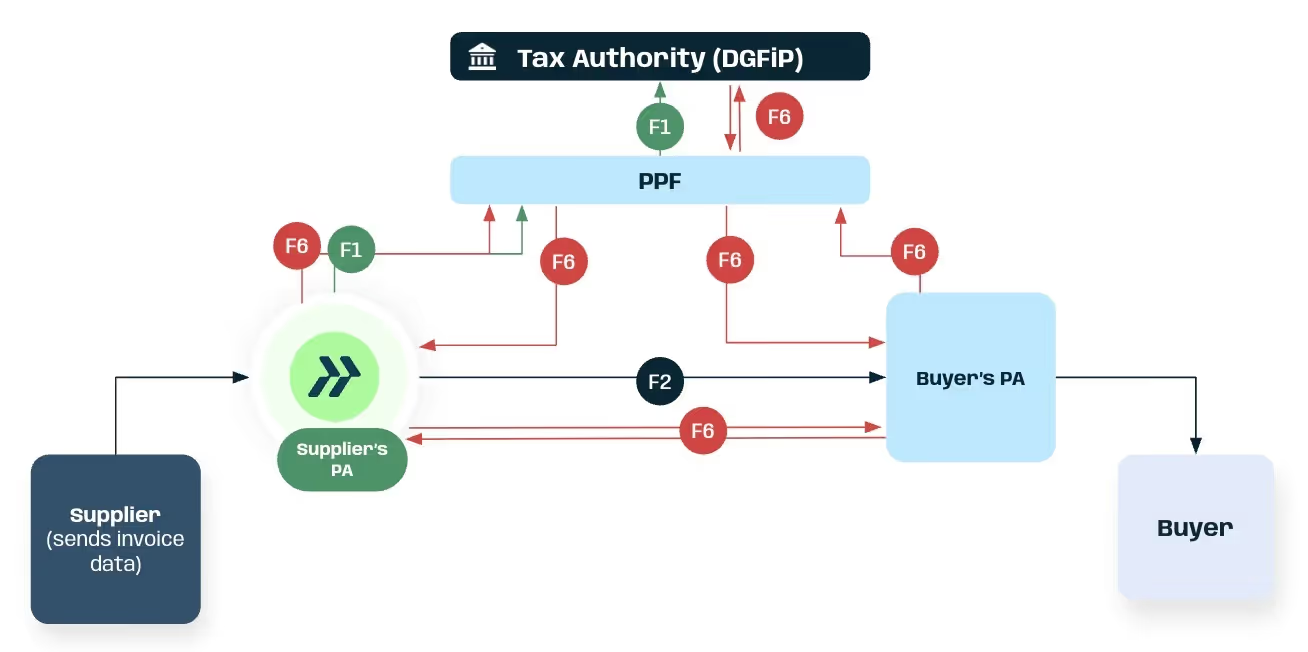

The supplier sends the mandatory invoice data to its chosen PA (PA-e). The platform validates the invoice format and performs the required regulatory checks. Using the Central Directory (Annuaire), the supplier’s platform identifies the buyer’s PA (PA-r) and routes the invoice accordingly (Flow 2). The PA-r performs its own validation checks and makes the invoice available to the customer.

At the same time, the PA-e transmits a defined subset of the invoice data to the Public Invoice Portal (PPF) (Flow 1). This ensures that the tax administration receives the required regulatory information without the full commercial invoice having to be centralized.

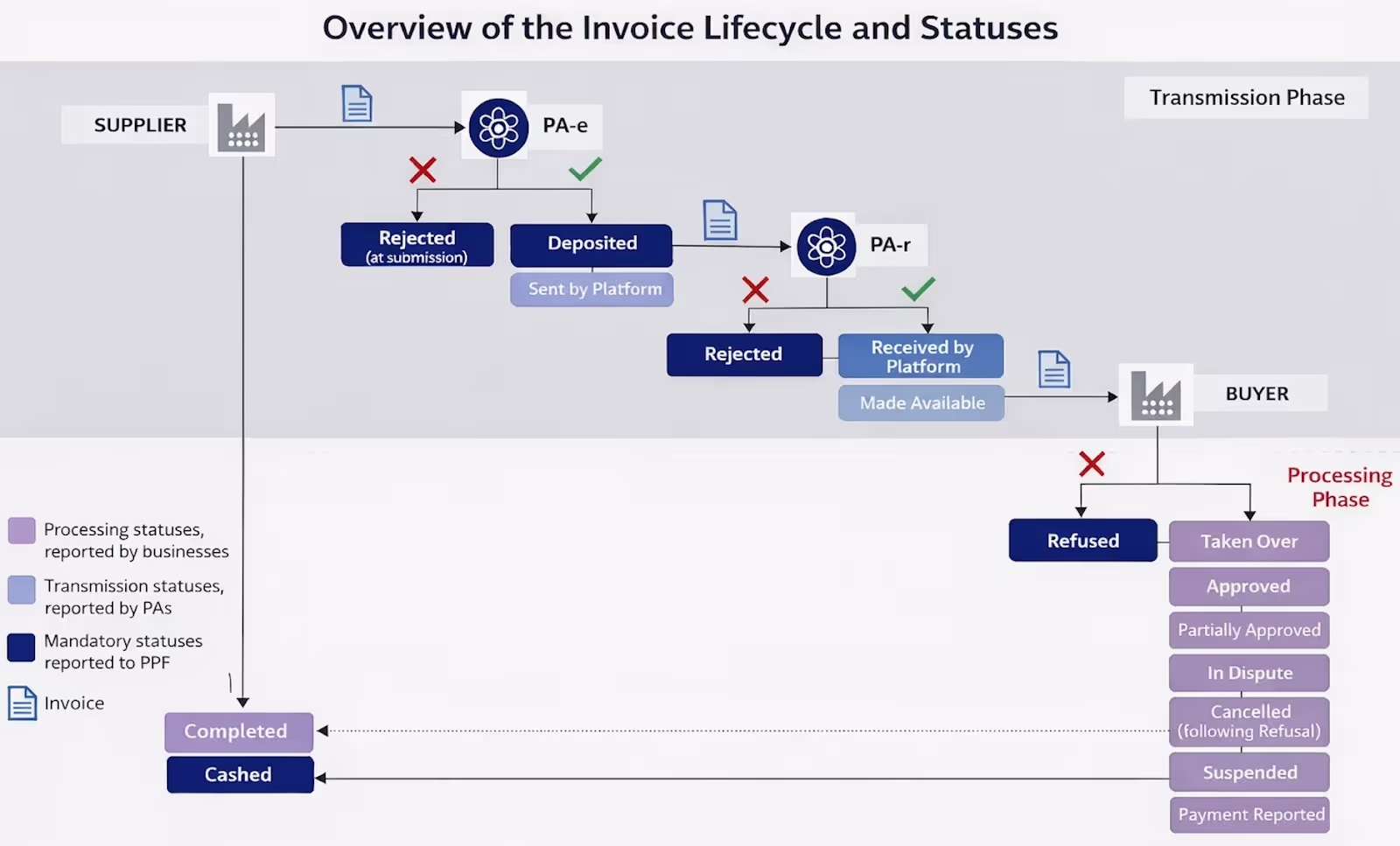

Invoice lifecycle statuses in the French e-invoicing reform

A major innovation of the reform is the structured lifecycle for invoices. Beyond simple transmission, invoices move through defined statuses. These include transmission-related statuses such as Deposited (Déposée), Received (Reçue) or Rejected (Rejetée), as well as business processing statuses such as Refused (Refusée), In dispute (En litige), or Cashed (Encaissée).

Importantly, four lifecycle statuses are mandatory and must be transmitted to the PPF: Deposited, Rejected, Refused, and Cashed. These mandatory status messages ensure that the tax administration is informed of key compliance events: from the initial submission of the invoice, through any technical rejection or commercial refusal, to confirmation of payment where relevant.

Note that the transmission of the "Cashed" status to the PPF is only mandatory in the following cases:

- For invoices corresponding to services where the supplier has not opted to pay VAT upon invoice issuance (TVA sur les débits).

- For invoices relating to down payments for either goods or services. VAT is always due upon the payment of an acompte, even if the supplier has generally opted for VAT on debits.

Operational edge cases in the French e-invoicing flow

While this represents the standard, nominal flow, the reform anticipates a variety of operational scenarios and edge cases.

What happens if the buyer has not selected an accredited platform

By law, all businesses must choose a platform to receive invoices. However, if a buyer is registered in the Central Directory but has not yet selected an Accredited Platform (PA-r), the supplier remains obligated to issue the electronic invoice. The supplier’s platform transmits the required data to the Public Invoice Portal and generates a "Deposited" status with the specific reason "NON_TRANSMISE" (not transmitted). This mechanism ensures that the supplier remains compliant even when the buyer has not completed their onboarding. Because the buyer is legally required to accept electronic invoices via an accredited platform, they cannot demand a paper or PDF invoice from the supplier as if they were exempt. The situation is treated as if the buyer simply "lost" the invoice. To get paid, the supplier can contact the buyer and send a duplicate outside the platform. If the buyer quickly sets up a platform, the supplier's PA-e can optionally replay the transmission so the invoice arrives properly through the regulated network.

What happens if a buyer is not listed in the PPF directory

The reform has introduced specific tolerances for edge cases where a buyer cannot be found in the directory. If a VAT-registered VAT taxable buyer is absent from the Central Directory due to administrative validation delays or technical issues on the government's end, the supplier is permitted to temporarily treat them as a non-taxable person. This same rule applies if the buyer is an entity without a SIREN number. In these cases, the supplier must fulfill their obligations using the B2C e-reporting flow rather than the B2B e-invoicing flow. The buyer will not be penalized for their absence from the directory, and the supplier will not face penalties for failing to issue a B2B e-invoice, provided they properly submit the B2C e-reporting data.

Frequently asked questions about the French e-invoicing flow

What is the French e-invoicing flow?

The French e-invoicing flow refers to the structured transmission process used to exchange electronic invoices between accredited platforms and report regulatory data to the tax administration through the Public Invoice Portal (PPF).

Which invoice formats are supported under the French e-invoicing reform?

The French reform allows three structured invoice formats:

- UBL (Universal Business Language)

- CII (Cross Industry Invoice / UN-CEFACT)

- Factur-X, a hybrid format combining a human-readable PDF with embedded structured XML data.

How are invoices transmitted in the French e-invoicing system?

Invoices are issued through an accredited platform (PA). The supplier’s platform validates the invoice, identifies the buyer’s platform through the Central Directory and routes the invoice accordingly. At the same time, regulatory invoice data is transmitted to the Public Invoice Portal.

What invoice lifecycle statuses must be transmitted to the Public Invoice Portal?

Four lifecycle statuses must be transmitted to the Public Invoice Portal:

- Deposited

- Rejected

- Refused

- Cashed (where applicable)

These statuses allow the tax administration to track key compliance events in the invoice lifecycle.

What happens if the buyer has not selected an accredited platform?

If the buyer has not yet selected an accredited platform, the supplier must still issue the electronic invoice. The supplier’s platform transmits the invoice data to the Public Invoice Portal and generates a “Deposited” status with the reason "NON_TRANSMISE".

What happens if a buyer is not listed in the PPF directory?

If a VAT taxable buyer cannot be found in the Central Directory due to administrative or technical issues, the supplier may temporarily treat them as a non-taxable person and submit the transaction through the B2C e-reporting flow instead of the B2B e-invoicing flow.

.webp)