In the previous post, we examined the architecture of the reform, the stakeholders involved, and how the e-invoicing flow operates in practice. We now move to the second pillar of the reform: the e-reporting flow.

Overview of the French e-reporting flow

E-reporting complements e-invoicing by capturing transactions that fall outside the domestic B2B exchange framework, namely B2C and cross-border B2B transactions.

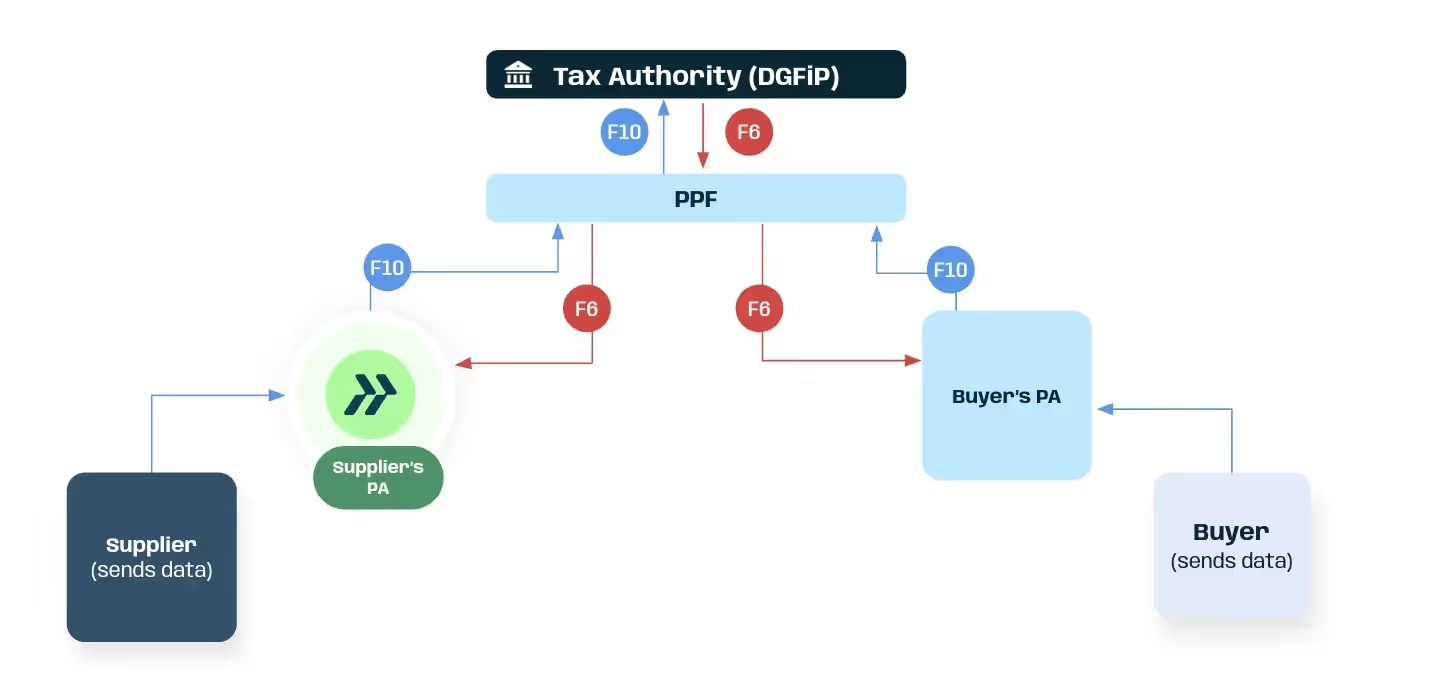

Under the French reform, all exchanges between Accredited Platforms (PAs) and the Public Invoice Portal (PPF) are organised into predefined transmission channels referred to as “flows.” Each flow corresponds to a specific type of data exchange; for example, one flow is used to transmit invoice data, another to report transaction data, and another to communicate status messages.

For B2C and cross-border transactions, rather than exchanging a structured e-invoice with a buyer, businesses must transmit the relevant transaction data and, in certain cases, payment data to the PPF through their chosen PA. This reporting transmission takes place via the dedicated reporting channel known as Flow 10 (F10).

Once a PA submits an F10 transmission to the PPF, the portal performs technical and functional controls. Based on the outcome of these checks, the transmission is either accepted or rejected. The PPF then sends a lifecycle message (Flow 6 – F6) back to the transmitting PA.

Importantly, in the e-reporting context, Flow 6 applies at the level of the transmission object (i.e., the entire F10 reporting file), not at the level of an individual invoice.

In other words:

- In e-invoicing, Flow 6 tracks the lifecycle statuses of a specific invoice (e.g., "Deposited", "Rejected", "Refused").

- In e-reporting, Flow 6 acts as a receipt, confirming whether the submitted transaction/payment dataset has been accepted or rejected by the PPF.

The reporting logic itself varies depending on the type of transaction (cross-border B2B, B2C, payment reporting). Accurate classification is therefore essential to determine the correct reporting method and frequency.

Cross-border B2B transaction reporting

Cross-border B2B transactions are reported at the invoice level. The reported data includes identification numbers, VAT amounts, applicable rates, countries of establishment, and invoice references. This ensures that transactions involving foreign counterparties are visible to the French administration, even though they are not exchanged within the domestic e-invoicing network.

B2C transaction reporting under the French reform

Transactions with private individuals or non-VAT-subject entities, both domestic and cross-border, are subject to e-reporting. Typically, B2C data is aggregated per day, including total amounts and VAT per rate. Crucially, no personal data about the consumer is ever transmitted to the PPF. Furthermore, recent simplifications mean businesses no longer need to report the exact number of daily transactions, nor do they need to submit "empty" reports for periods where no sales occurred.

Payment reporting requirements in the French e-reporting system

Where VAT is due upon receipt of payment (TVA sur les encaissements), payment data must also be transmitted to the PPF. This obligation only applies to services, provided that the company has not opted for VAT payment on an accrual basis or is required to self-assess VAT.

The reporting trigger is the date the funds are received, not the invoice date, and the obligation to report falls on the supplier receiving the payment.

If the payment relates to a domestic B2B electronic invoice, the payment information is transmitted via the “Cashed” lifecycle status.

If the payment relates to cross-border transactions or B2C transactions, reporting occurs periodically and, for B2C transactions, in aggregated form.

E-reporting frequency and reporting deadlines

Reporting frequency depends on the VAT regime of the business. For example, taxpayers under the standard monthly VAT regime are required to report their transaction data three times a month (every 10 days), but their payment data only once a month. Other businesses, such as those under a simplified regime or benefiting from the basic VAT franchise, may report transaction and payment data monthly or bimonthly. The submission deadline is generally 10 days after the end of each period, and these deadlines must be strictly observed.

Frequently asked questions about the French e-reporting flow

What is e-reporting in the French e-invoicing reform?

E-reporting is the mechanism used to report transaction data to the tax administration for transactions that fall outside domestic B2B e-invoicing. This includes B2C transactions, cross-border B2B transactions and certain payment data.

Which transactions must be reported under French e-reporting?

E-reporting applies to:

- B2C transactions (domestic and cross-border)

- Cross-border B2B transactions

- Certain payment data where VAT is due upon receipt of payment.

What is Flow 10 in the French e-reporting system?

Flow 10 (F10) is the transmission channel used to submit transaction and payment data from an accredited platform to the Public Invoice Portal (PPF).

What is Flow 6 in the French e-reporting process?

Flow 6 (F6) is the lifecycle message returned by the Public Invoice Portal confirming whether the submitted reporting file has been accepted or rejected.

How often must businesses submit e-reporting data in France?

Reporting frequency depends on the VAT regime. Businesses under the standard monthly VAT regime generally report transaction data three times per month and payment data once per month.

Is personal data reported for B2C transactions?

No. The French reform does not require personal data about consumers to be transmitted. B2C reporting is typically aggregated per day and includes totals and VAT amounts per rate.

.webp)