Introduction to the Reverse Charge Mechanism

The reverse charge mechanism is a VAT process where the buyer, not the seller, pays VAT directly to the government. Post-Brexit, UK businesses trading with EU entities must check updated VAT rules to ensure correct application. This mechanism primarily applies to cross-border B2B transactions and certain domestic B2B scenarios to prevent tax fraud.

The Reverse Charge Mechanism: Pre- and Post-Brexit

The European Union’s (EU) cross-border reverse charge mechanism is a fundamental aspect of intra-EU trade in goods and services which applies to many transactions between businesses in different EU member states.

However, since the United Kingdom (UK) left the EU on 1 January 2021 (i.e. after Brexit).

- The scope and application of the cross-border reverse charge mechanism between the UK and the EU have changed.

- Businesses must ensure compliance with new VAT rules tailored to post-Brexit trade.

Why Post-Brexit VAT Rules Matter

If you are a business selling to or from the UK, you should double-check that you apply the correct VAT rules to your transactions after Brexit, specifically concerning the reverse charge.

This article provides:

- A breakdown of how the reverse charge mechanism works in the UK today.

- A summary of the fundamental changes that have occurred since Brexit.

- Insights into some of the more unusual aspects of the UK Reverse Charge.

Understanding the VAT Reverse Charge Mechanism

Before exploring the changes in the UK, let's remind ourselves about the reverse charge:

What is the Reverse Charge?

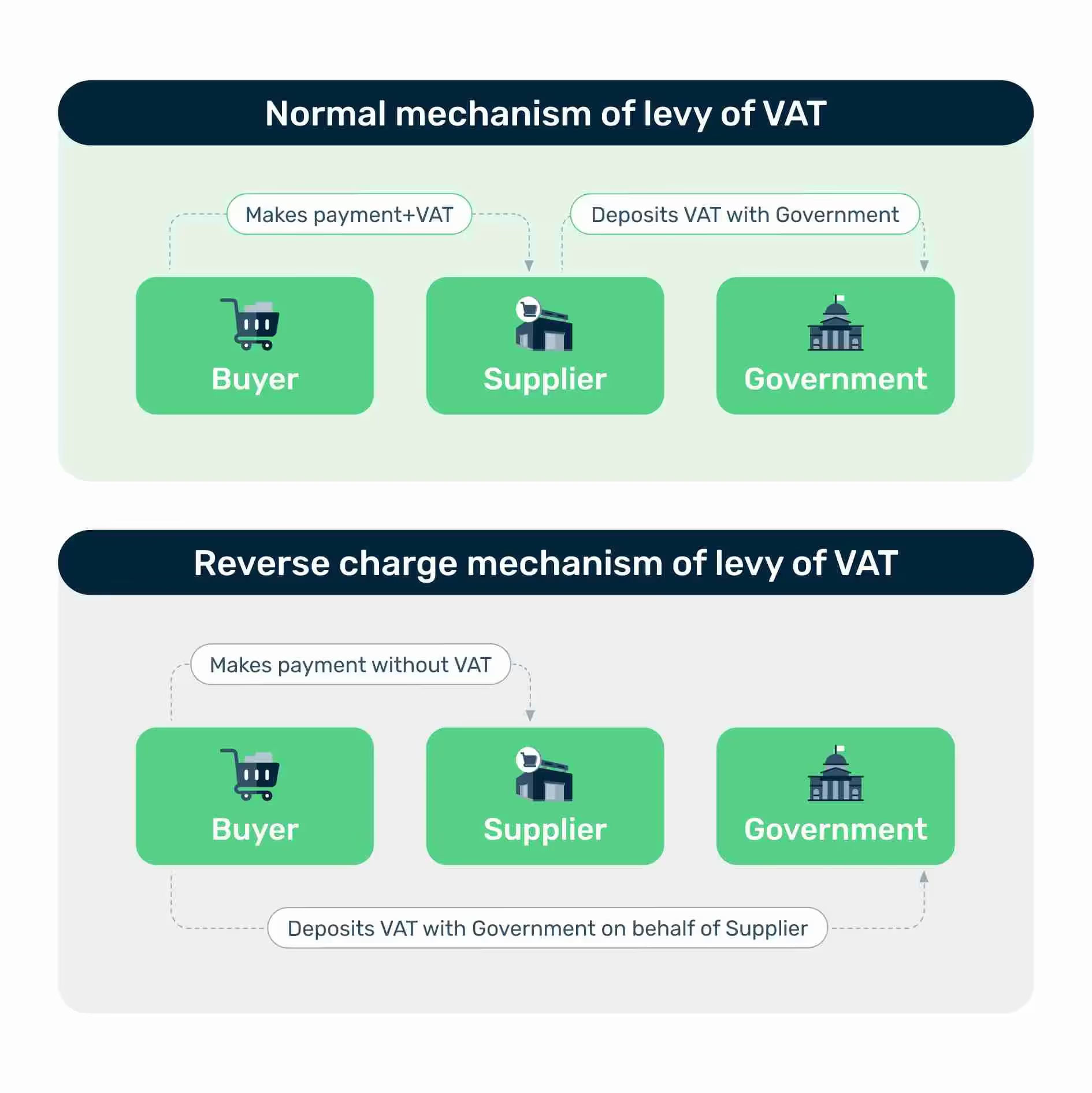

The reverse charge mechanism is a process in which the value-added tax (VAT) is paid to the government by the buyer and not the seller, unlike in the case of normal VAT rules.

When Does the VAT Reverse Charge Apply?

The reverse charge mechanism typically applies in the case of taxable supplies of goods or services in cross-border, business-to-business (B2B) transaction scenarios. In most countries, the mechanism is also used in a few specific domestic B2B transaction types prone to tax fraud. The reverse charge mechanism never applies when selling to non-business consumers (i.e., end users) save for some very exotic cases.

How the VAT Reverse Charge Works in the UK

Under the reverse charge mechanism, the buyer is responsible for directly declaring and paying VAT due on a transaction to the tax authorities. The supplier typically issues an invoice without VAT and makes the relevant reference to the reverse charge mechanism on it. The reverse charge rules are based on the place of supply rules for goods and services. One note is that the reverse charge mechanism does not apply in the case of a zero-rated supply of services. When the reverse charge mechanism applies to a transaction, the buyer must apply (“self-assess”) the same rate of VAT that would apply if it was a domestic transaction.

Example of the Reverse Charge Mechanism

Let’s look at a cross-border supply of services in a B2B scenario:

- You are a VAT-registered business established in the UK buying services from a German company for £100. In this case, the German company issues an invoice for £100 with no VAT applied.

- Once you receive the invoice, you must assess your VAT obligation by applying the same VAT rate to the purchase that would apply if you purchased the same services from a UK company, e.g., the standard 20% UK VAT rate.

- Now you need to account for the resulting £20 VAT liability in your VAT return. Nonetheless, the reverse charge mechanism's economic effect on your VAT liability is typically neutral, as the VAT payable can usually be offset by the input VAT credit claimed on the same VAT return without affecting the VAT payment obligation.

An unusual aspect of the UK Reverse Charge Mechanism

One lesser-known fact about the UK reverse charge is that this mechanism can apply to sales of services made to VAT-unregistered businesses. Where the UK entrepreneur is not registered for UK VAT, the value of the supply will count towards the unregistered business's VAT registration turnover threshold. For example - if a UK VAT unregistered business buys GBP85,000 worth of services from abroad on which it would typically self-assess VAT, this purchase would mean that the business has now exceeded the VAT registration threshold.

More information about this can be found in HMRC guidelines and examples. Notably, the UK was not the only jurisdiction with such a rule - at least one other EU Member State still has a similar quirk in its implementation of the VAT Directive.

If you need a broader reminder about the reverse charge, we have written a handful of articles on this topic that explore the concept in more depth:

- The Reverse Charge Mechanism: What You Need to Know

- EU Reverse Charge: What Is It And Who Is It For?

- How do you say “Reverse-Charge” in other European Languages?

What changed in the UK reverse charge after Brexit?

Following the exit of Britain from the European Union, the application of the reverse charge procedure for intra-EU business-to-business (B2B) sales has changed.

After Brexit, Great Britain (consisting of England, Scotland, and Wales) is no longer treated as an EU Member state and has stopped applying the reverse charge to EU sales of goods and services. Northern Ireland continues to be treated as an EU Member State with regard to VAT on goods and, therefore, continues to apply the EU reverse charge for goods.

EU Businesses trading with the UK and vice versa will no longer have the same rules relating to the reverse charge as before Brexit. They will need to be aware of the fundamental changes that took place. Let's look at the implication from the point of view of selling into the UK and from the UK in turn.

What is the Northern Ireland Protocol?

The Northern Ireland Protocol is an agreement that forms part of the broader Brexit withdrawal agreement between the United Kingdom (UK) and the European Union (EU). It was designed to address the unique circumstances of Northern Ireland, which shares a border with the Republic of Ireland (an EU member state) while also being part of the UK.

The protocol aims to avoid the need for a physical border between Northern Ireland and the Republic of Ireland, thus preserving the peace and stability achieved through the Good Friday Agreement. It achieves this by creating a regulatory and customs border down the Irish Sea, with Northern Ireland effectively remaining in the EU's single market for goods and aligning with certain EU rules to avoid customs checks at the Irish border.

The protocol ensures that Northern Ireland aligns with EU VAT rules for goods while remaining part of the UK's VAT system. UK VAT rules for services apply throughout the UK, with HMRC responsible for VAT operation and revenue collection in Northern Ireland.

Under the Protocol, VAT applies to goods entering Northern Ireland from Great Britain and vice versa. However, certain flexibilities within EU VAT rules have been utilized to minimize business impact.

Registration for VAT in Northern Ireland remains within the UK's VAT system, and existing VAT registration is unaffected.

How does VAT between the UK and EU work after Brexit?

Here is a summary of the key VAT considerations when conducting trade between the UK and the EU. Particular attention has been given to the special rules surrounding Northern Ireland.

Selling goods and services from the EU to Great Britain (England, Scotland, and Wales) - not Northern Ireland

- Sellers should consider the transaction as an export of goods or a supply of services to a third territory.

- EC Sales and Intrastat declarations are no longer required for sales of goods or services to Great Britain.

- VAT-registered businesses in the UK receiving services from EU businesses must still apply the reverse charge mechanism and self-assess the VAT payable on the transaction.

- Sales of digital services to consumers (B2C) are no longer reportable through the Mini-One-Stop-Shop (MOSS), and businesses outside the UK must register for UK VAT if the supplies are liable to UK VAT.

- Intra-EU simplifications, such as triangulation and call-off stock, are unavailable for goods involving Great Britain.

Selling goods and services from the EU to Northern Ireland

- Northern Ireland is still treated as an EU member for goods trade, and EC Sales and Intrastat declarations are still necessary.

- The VIES system with the prefix "XI" can check VAT numbers in Northern Ireland.

- Selling services to Northern Ireland is treated the same as selling services to other parts of the UK, and the reverse charge does not apply.

- Sales of digital services to consumers (B2C) are no longer reportable through MOSS, and businesses outside the UK must register for UK VAT if the supplies are liable to UK VAT and sold to consumers in Northern Ireland.

- Intra-EU simplifications, such as triangulation and call-off stock, remain available for Northern Ireland and EU member states.

Selling goods and services from the UK to the EU

- Selling goods to the EU from Great Britain (England, Scotland, Wales) is considered an export or supply to a third territory.

- An EORI number is required for businesses in Great Britain selling or moving goods to the EU.

- Import VAT may need to be paid upon importation of goods into the EU from Great Britain.

- MOSS simplification can no longer be used for sales of digital services from the UK to the EU.

- Intra-EU simplifications, such as triangulation and call-off stock, are unavailable for goods involving Great Britain.

Selling goods and services from Northern Ireland to the EU

- Northern Ireland is still considered an EU member for goods trade, and EC Sales and Intrastat declarations are necessary.

- Selling services from Northern Ireland is treated like selling services from other parts of the UK, and the reverse charge does not apply.

- VAT treatment for goods transported via Northern Ireland to an EU member state depends on specific circumstances and the location of the transfer of rights to the goods.

- Intra-EU simplifications, such as triangulation and call-off stock, remain available for Northern Ireland and EU member states.

What happens to sales and movements of goods between Great Britain and Northern Ireland?

VAT on goods sold between Great Britain and Northern Ireland is charged by the seller and accounted for as output VAT. Exceptions apply to special customs procedures, domestic reverse charge rules, onward supply procedures, and online marketplace sales.

For businesses moving their own goods between Great Britain and Northern Ireland, VAT is due and should be accounted for as output VAT. Input VAT recovery is subject to standard rules. Similar principles apply when goods are moved from Northern Ireland to Great Britain.

Sales of goods from Great Britain to Northern Ireland, and within Northern Ireland, by UK VAT group members follow specific rules. VAT Retail Export Scheme (RES) operates in Northern Ireland, allowing retailers to offer VAT refunds to visitors. Personal exports of vehicles from Northern Ireland to Great Britain and sales of goods on board ferries are subject to specific VAT rules.

What happened to EC Sales Lists after Brexit?

Generally, businesses in England, Scotland and Wales will no longer need to complete an EC Sales List as these territories are no longer part of the EU. However, businesses in Northern Ireland selling goods into Europe must file an EC Sales List. For more information on how to complete the EC Sales List, please see these HMRC guidelines.

What happened to Intrastat declarations after Brexit?

Intrastat registration and declaration are not required for goods transported between Great Britain (England, Wales, and Scotland) and the EU or between Great Britain and Northern Ireland.,

Registration is only required when within a given calendar year (from January 1st to December 31st), your business meets either of the following criteria:

- If the value of goods received from the EU into Northern Ireland exceeds £500,000.

- If the value of goods moved from Northern Ireland to the EU exceeds £250,000.

For more information, please see HMRC guidelines.

What is postponed VAT Accounting

Imports into the UK require taxes to be paid on import. This has a significant impact as paying VAT on all imports up front would be a significant cash flow burden for most businesses. To address this, HMRC has introduced “postponed VAT accounting”. Under postponed VAT accounting, you can account for your import VAT in your VAT return. This way, you can declare and recover the import VAT in one motion, as you would with input tax. You can utilize postponed VAT accounting if:

- You are a VAT-registered business in the UK

- The imported goods serve a business purpose

- Your VAT number is included in your import declaration

You can learn about postponed VAT accounting by consulting this HMRC guidance.

Do I need an EORI number after Brexit?

If you are moving goods to or from Northern Ireland, you will typically require an EORI (Economic Operators Registration and Identification) number starting with "XI." This applies to various activities such as importing goods from Great Britain to Northern Ireland, exporting goods from Northern Ireland to a non-EU country, making declarations, or applying for customs decisions in Northern Ireland. However, if you only move certain goods from Northern Ireland to Great Britain, you may need to make an export declaration and have an EORI number that starts with "XI".

- For more information about EORI numbers, please consult these guidelines.

- To apply for an EORI number, please you can start your application here.

What happened to the VAT MOSS after Brexit?

The VAT Mini One Stop Shop (MOSS) was a nifty scheme that allowed businesses registered for VAT MOSS in an EU country to effortlessly offer digital services to consumers in other EU countries without the hassle of registering in each individual country. Unfortunately, this convenient scheme is no longer accessible in the UK after Brexit.

If your business provides eligible digital services in the EU, you'll need to explore alternatives, such as registering for VAT MOSS in another EU country or tackling the administrative burden of registering and collecting VAT in every country you operate in.

To learn about how to pay VAT when you sell digital services today, you can consult these guides:

- Selling to EU consumers

- Selling to UK consumers.

How can I validate a Northern Ireland VAT number?

From January 1, 2021, the VIES on the Web service for validating UK (GB) VAT numbers is no longer available. A new service was introduced to validate VAT numbers for businesses operating under the Protocol on Ireland and Northern Ireland. These VAT numbers have a prefix of "XI" and can be found in the "Member State / Northern Ireland" dropdown menu under the new entry "XI-Northern Ireland."

Traders who need to validate UK (GB) VAT numbers can make their request to the UK Tax Administration.

What happened to the UK Domestic Reverse Charge after Brexit?

There has not been a material impact on the Domestic Reverse charge due to Brexit. In special cases, the reverse charge mechanism also applies to domestic B2B transactions within the UK. These transaction types are especially prone to VAT fraud. The reverse charge mechanism makes it significantly harder for criminals to take advantage of the VAT system. In the case of a VAT reverse charge, the seller cannot disappear with the amount of VAT collected as the buyer pays it. Besides helping the government combat VAT fraud, the domestic reverse charge benefits the entire supply chain for the same reasons.

The UK has a specific list of goods and services where the domestic reverse charge VAT treatment must be applied.

The specified goods that the reverse charge applies to are:

- mobile phones

- computer chips

- wholesale gas

- wholesale electricity

The specified services are:

- emission allowances

- wholesale telecommunications

- renewable energy certificates, and

- supplies of construction services

You can find further information about the specific definitions of the transaction types listed above in this HMRC guidance.

When making a sale that falls in the scope of the VAT domestic reverse charge mechanism, you must apply some additional wording on the respective VAT invoice. HM Revenue provides guidance on these additional requirements. In essence, you would need to indicate that the supplies are subject to domestic reverse charge, the amount of VAT, and that the buyer is obligated to pay this VAT to HMRC.

To get information about what type of construction services fall under reverse charge rules, consult HMRC’s guidance on the construction industry scheme (CIS).

Key Takeaways on the VAT Reverse Charge Mechanism

The key takeaway from this article is that since Brexit, the application of the reverse charge mechanism between the UK and the EU has changed. Businesses involved in cross-border trade between the UK and the EU must be aware of the changes in the reverse charge mechanism and VAT rules to ensure compliance and avoid disruptions in their operations.

- Great Britain (England, Scotland, and Wales) is no longer treated as an EU member state and has stopped applying the reverse charge to EU sales of goods and services.

- Northern Ireland continues to be treated as an EU member state with regard to VAT on goods, and the reverse charge still applies for goods traded with the EU.

- This also has knock-on effects for EC Sales listings, Intrastat declarations, the Mini One Stop Shop scheme, postponed VAT accounting, and the EORI requirements.

If you are interested to learn more about the UK VAT, here are some more resources:

- VAT Invoice Requirements in the United Kingdom

- UK VAT Guide: Tax Number Format, Rates & Compliance

- VAT on Digital Services in the United Kingdom

- E-invoicing in the United Kingdom

How can Fonoa help?

Knowing when you should or shouldn’t charge VAT on your cross-border sales is crucial for staying tax-compliant. With Fonoa Lookup, you can:

- Validate tax IDs across the globe: Instantly validate tax IDs in 100+ countries and understand if you're selling to B2B or B2C.

- Comprehensive results: Retrieve the most comprehensive information related to tax IDs directly from government sources.

- Simple access and flexible usability: Monitor and review validations from a simple, intuitive user interface or integrate directly through our API.

Applying the reverse charge mechanism correctly in your accounting software can be challenging.

Adopting best practices and applying lessons learned from the world’s leading digital companies will accelerate your success. The team of tax experts at Fonoa works with many leading companies to optimize their VAT compliance process while making tax digital for them and can help answer your VAT compliance questions. Please reach out if you want to learn more or discuss how our tax experts can help you automate your VAT compliance process.